“Is that to say we are against Free Trade? No, we are for Free Trade, because by Free Trade all economical laws, with their most astounding contradictions, will act upon a larger scale, upon the territory of the whole earth; and because from the uniting of all these contradictions in a single group, where they will stand face to face, will result the struggle which will itself eventuate in the emancipation of the proletariat.”

Karl Heinrich Marx · Marx-Engels Collected Works, Vol. VI, p. 290

You can also find this library at CRAN and download it directly from R and RStudio.

Also, we recommend viewing the mind map summary at the end of the article to better understand the relationship between the functions of the package.

LISTEN TO THIS POST AS A PODCAST:

ESCUCHA ESTA PUBLICACIÓN COMO PODCAST

R Library Review

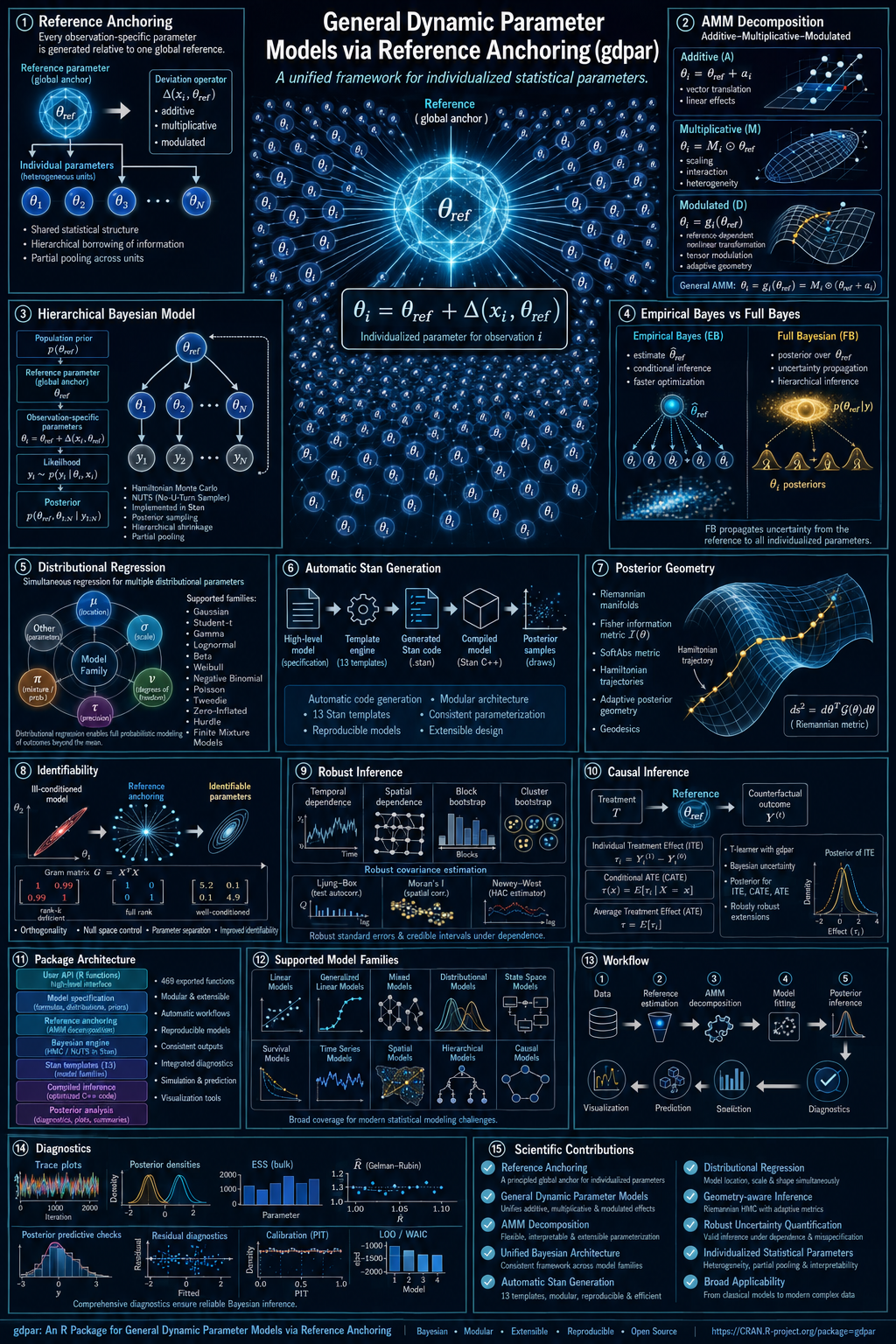

Meet gdpar

General Dynamic Parameter Models via Reference Anchoring

In the fleeting calculus of a two-second decision—overtaking a car on a narrow road—the human brain performs a remarkable statistical trick. It does not build a model of the approaching driver from scratch. Instead, it retrieves a baseline: the average driver, representing typical reaction times and modal aggression. In a split second, it reads the specific signals of the actual driver—relative speed, vehicle type, micro-movements—and estimates how this specific driver deviates from the baseline. The decision to overtake emerges from that synthesis.

This cognitive recipe—population reference + individual deviation—is the philosophical bedrock of the R package gdpar (General Dynamic Parameter models via Reference Anchoring) by José Mauricio Gómez Julián. The package takes this intuition, formalizes it as a rigorous statistical decomposition, proves the conditions under which it is mathematically identifiable, ships a Stan-based Bayesian engine to estimate it, and layers on causal inference, geometry-adaptive sampling, and dependence-robust inference.

❦

The Anatomy of Deviation

Every layer of gdpar is an elaboration of a single, elegant equation. For each observation $i$ with covariates $x_i$:

Read it as: the parameter of individual $i$ equals a population reference, plus a deviation that is itself a function of the individual’s covariates and of the reference itself.

That final clause is where the architecture pivots from classical statistics. The deviation $\Delta$ does not merely depend on who you are (your covariates $x_i$); it depends on what the reference is. If you transplant the model to a new population, the deviation function behaves differently because $\theta_{\text{ref}}$ is one of its arguments. This structural dependence is the defining feature of “reference anchoring.” It distinguishes gdpar from random-effects or varying-coefficient models, where the deviation is structurally separate from the reference.

So, what is the shape of $\Delta$? The package singles out a specific functional form called the Additive–Multiplicative–Modulated (AMM) decomposition:

Three mechanisms, cleanly separated and independently interpretable:

$a(x)$ — A pure additive shift. Think of this as a traditional fixed-effect driven by covariates.

$b(x)\odot\theta_{\text{ref}}$ — A covariate-dependent scaling of the reference (using the Hadamard/elementwise product). This is where “the deviation depends on the reference” enters multiplicatively.

$W(\theta_{\text{ref}})\,x$ — Covariates are mixed through a matrix $W$ that is, itself, tuned by the reference. This is the explicit, structural reference-dependent channel.

Standard models drop out as special cases. Set $\Delta \equiv 0$ and you have fixed-effects regression. Set $W \equiv 0$ and you have a hierarchical model with multiplicative interaction. Set $b \equiv 0$ and you have a varying-coefficient model. The AMM is the smallest natural family that contains all three and elevates the reference to an active argument of the deviation.

❦

The Three Estimation Engines

gdpar defines three complementary engines for estimating $\Delta$. Crucially, only one is executable in the current release—a deliberate choice to promise a mathematical scope that exceeds the executable surface, and to say so honestly.

Path

Engine

Representation

Status

Path 1

Hierarchical Bayesian (Stan)

Parametric AMM

✅ Operational

Path 2

Varying-coefficient (splines)

Smooth $\beta(z)$

🚧 Conceptual

Path 3

Hypernetwork / Neural Net

Net generates $\theta_i$

🚧 Conceptual

Paths 2 and 3 are documented to “reference grade”—full asymptotic theory (contraction rates, Bernstein–von Mises) is developed in the Wiki—but they abort with gdpar_unsupported_feature_error if invoked. Path 1 places priors on every component ($\theta_{\text{ref}}, a, b, W$) and samples the joint posterior with HMC, yielding native, full-posterior uncertainty.

A Tale of Two Posteriors: EB vs. FB

Within Path 1, gdpar offers two inferential regimes. Full Bayes (FB) via gdpar() samples the joint posterior, remaining most faithful to the cognitive analogy. Empirical Bayes (EB) via gdpar_eb() estimates the hyperparameters by maximizing a marginal likelihood via a Laplace approximation, then samples the remaining parameters conditionally.

The EB vs FB Comparator

Rather than forcing a choice, gdpar treats them as parallel routes. It ships a dedicated comparator, gdpar_compare_eb_fb(), which quantifies agreement on $\theta_{\text{ref}}$ and the reduced parameter vector $\xi$. The Wiki develops the theory to first-class depth: EB and FB lower-level posteriors agree asymptotically (Theorem 7A), while EB intervals under-cover by $O(n^{-1})$ (Proposition 7B). If you have ever wondered if EB is “good enough” for your data, gdpar lets you answer that empirically.

Distributional Regression: Every Parameter is a Slot

gdpar is not constrained to modeling the mean. A probability distribution has multiple parameters—location, scale, shape, tail index, zero-inflation probability—and each one can carry its own AMM decomposition. The package indexes these by $k = 1, \dots, K$:

$$ \theta_i^{(k)} = \theta_{\text{ref}}^{(k)} + \Delta^{(k)}(x_i, \theta_{\text{ref}}^{(k)}), \qquad k = 1, \dots, K $$

The built-in roster covers Gaussian, Poisson, negative binomial, Bernoulli, Beta, Gamma, Student-$t$, Tweedie, ZIP, ZINB, and hurdle families. Zero-inflated and hurdle models receive an especially elegant treatment: both the zero-inflation probability $\pi_i$ and the count parameter $\theta_i$ are anchored to their respective references—a dual deviation design.

❦

The Causal Bridge

Because the AMM form produces individual parameters, individual treatment effects emerge naturally. gdpar_causal_bridge() implements a T-learner: fit the anchored model separately under treatment and control, then read the conditional average treatment effect (CATE) at $x_i$ as the difference of the anchored individual predictions:

A second layer, gdpar_compare_meta_learners(), benchmarks the AMM-based learner against external meta-learners via pluggable adapters: grf::causal_forest on the R side and EconML’s CausalForestDML on the Python side (via reticulate). The framework’s causal claims are benchmarked, not asserted.

Mechanics & Clockwork

Several engineering decisions elevate gdpar from a theoretical exercise to a serious computational environment:

Stan Code Generator: Composes programs from canonical pieces—AMM blocks for $p=1$ and $p \geq 1$, EB marginal/conditional blocks, distributional-$K$ blocks—selected by the resolved $(K, p, \text{family}, W, \text{parametrization}, \text{group})$. The $W$ basis supports B-splines with Stan-side Cox–de Boor evaluation, ensuring differentiability inside HMC.

Identifiability Pre-flight: Before any sampling, gdpar_check_identifiability() runs a Gram-matrix check (Proposition 1C), a per-coordinate cross-component check (C4-bis) for $p > 1$, and a per-group anti-aliasing check (C7). If your design is non-identifiable, you find out before the sampler burns your CPU, accompanied by a structured gdpar_identifiability_error naming the dependent directions.

Data-Driven Reparametrization: Treats the parametrization of $b(x) \odot \theta_{\text{ref}}$ as a pre-fit decision. A short pilot computes an information ratio, dispatching to CP, NCP, or—gdpar‘s root-cause resolution—a linear reparametrization that samples the product $\theta_{\text{ref}} \cdot b$ directly, sidestepping bilinear funnels altogether.

Opt-in Power Tools

Two advanced capabilities are switched off by default, documented as thoroughly as the core path.

1. Geometry-Adaptive Sampling

Hierarchical AMM posteriors can be geometrically hostile—funnels, near-determinism, heavy tails. The opt-in geometry engine climbs a ladder of Riemannian metrics: Euclidean → Fisher/SoftAbs → sub-Riemannian → relativistic/Finsler. A certifying orchestrator diagnoses the pathology, selects a metric, tunes the integrator, and emits a certificate. If full sampling is certified infeasible, a Laplace fallback provides a plug-in posterior with ELPD on par with mgcv-REML or INLA-Laplace.

2. Dependence-Robust Inference

gdpar does not model temporal or spatial dependence in its point structure; instead, it makes the inference robust to dependence (a working-independence + sandwich-variance stance in the spirit of Liang & Zeger, 1986). You receive diagnostics (Durbin–Watson, Ljung–Box, Moran’s $I$) and robust SEs via block bootstrap—moving or circular blocks in time (with the Politis–White flat-top automatic block length), tiled randomized-origin blocks in space. Point estimates remain pristine; only the uncertainty is made honest.

⚠️ Honest Limitations

The Wiki is admirably forthright about scope. Only Path 1 is executable in 0.1.0. Dependence is not modelled—only the inference is made robust. The package’s mathematical scope exceeds its executable surface by design. Read the “Implementation status” notes carefully before relying on a feature.

❦

TL;DR

gdpar takes one of the most natural ideas in human prediction—predict an individual as a deviation from a population reference, where the deviation itself depends on the reference—and transforms it into a fully specified, identifiability-checked, Stan-powered Bayesian regression framework. It is theoretically rigorous, computationally serious, and unusually honest about what it does and does not yet do. If your work involves individual heterogeneity, distributional regression, or causal effect estimation with principled uncertainty, gdpar demands a careful look.

You can also find this libraryat CRAN and download it directly from R and RStudio.

LISTEN TO THIS POST AS A PODCAST:

The Problem Every Quantitative Researcher Knows

Imagine you are staring at a spreadsheet with 50 columns and a few hundred rows of macroeconomic indicators. Somewhere inside this matrix, a handful of variables carry the signal you care about. The rest is noise — or worse, confounding variation that masquerades as signal. You need to answer three questions: Which variables actually matter? What is the latent structure driving them? And how persistent are the components you extract?

If you have worked with panel data for any length of time, you know that these questions are rarely addressed by a single tool. You run a LASSO in one environment, a PCA in another, an ADF test in a third. Each method lives in a different package with different input formats, different assumptions, and different output structures. Stitching the results together is left to you.

SignalY is an R package that was built to solve exactly this fragmentation problem. Developed by José Mauricio Gómez Julián and released under the MIT license, it provides a unified framework for signal extraction from panel data through multivariate time series analysis. Its design rests on three analytical pillars — column selection, series decomposition, and persistence analysis — that can be used independently or chained together through a single orchestrating function.

This post walks through the problem SignalY solves, the methods it implements, and why the combination matters for applied econometrics and data science.

Pillar 1: Which Variables Matter?

The first challenge in any high-dimensional analysis is selection. When you have dozens of potential predictors, you need a principled way to determine which ones carry structural information and which ones are along for the ride.

The Horseshoe Prior

SignalY approaches this problem through Bayesian sparse regression with the Horseshoe prior. The Horseshoe, introduced by Carvalho, Polson, and Scott (2010) and refined for practical variable selection by Piironen and Vehtari (2017), is a global-local shrinkage prior with a distinctive property: it is aggressive around zero (shrinking noise variables strongly toward zero) while maintaining heavy tails (allowing true signals to escape shrinkage). This dual behavior makes it particularly well-suited for sparse problems where you expect only a few variables to matter, but you do not know which ones.

The math behind this is elegant. Each coefficient βⱼ is given a prior with two layers of shrinkage:

A local parameter λⱼ that controls how much each individual coefficient is shrunk.

A global parameter τ that governs overall sparsity.

The result is a shrinkage profile where most coefficients collapse toward zero — the global pull — while a small number of coefficients stand apart, barely affected — the local escape. This is what gives the Horseshoe its name: the prior density looks like the shape of a horseshoe, with a sharp spike at zero and long, flat arms extending outward.

SignalY’s fit_horseshoe() function estimates this model and provides built-in shrinkage profile diagnostics, so you can visually inspect which variables survived shrinkage and by how much.

Four Ways to Select Variables

Fitting a model is one thing; converting the posterior into a concrete variable selection is another. SignalY offers four distinct selection strategies, each with different strengths:

Projection predictive selection (select_by_projection()): This is the most theoretically robust approach. It works by projecting the full posterior onto candidate submodels and selecting the smallest submodel whose predictive distribution is close enough to the full model. The reference is Piironen and Vehtari (2017), and the implementation respects the posterior geometry rather than relying on ad-hoc thresholds.

Credible interval exclusion (select_by_credible_interval()): Selects variables whose posterior credible intervals do not include zero. Intuitive and easy to interpret, though it can be conservative in high-dimensional settings.

Shrinkage-based selection (select_by_shrinkage()): Uses the kappa (shrinkage fraction) parameters to identify variables that escaped shrinkage. This is useful when you want to understand the degree of shrinkage, not just the binary in-or-out question.

Magnitude-based screening (select_by_magnitude()): A straightforward effect-size filter. Useful as a first pass or when you need to combine Bayesian inference with a frequentist-style screening step.

The fact that SignalY provides all four in a coherent pipeline — not as separate, unrelated functions — is the key design decision. You can run all four and cross-validate the results, or choose the one that best matches your inferential philosophy.

Beyond Regression: Factor Discovery

Sometimes the question is not “which of my 50 variables matter?” but rather “what are the few latent factors driving all 50?” SignalY addresses this through two complementary methods:

PCA with block bootstrap (pca_bootstrap()): Standard principal component analysis, but with block bootstrap confidence intervals that account for temporal dependence in time series data. It also includes entropy-based topology analysis, which measures the informational content of each component.

Dynamic Factor Models (estimate_dfm()): Implements the Bai and Ng (2002) information criteria for automatic determination of the number of static factors, then fits a VAR (Vector Autoregression) on the factor dynamics. This captures not just what the latent factors are, but how they evolve over time.

Pillar 2: What Is the Underlying Structure?

Once you know which variables matter (or have constructed a composite signal), the next question is decomposition: what are the trend, cycle, and residual components of your series?

This is where signal processing meets econometrics, and SignalY implements three methodologically distinct approaches, each with its own strengths.

Wavelet Decomposition

filter_wavelet() implements the Maximal Overlap Discrete Wavelet Transform (MODWT) using Daubechies wavelets, following the framework of Percival and Walden (2000).

Unlike a Fourier transform, which decomposes a signal into infinite sinusoids (losing all time information), a wavelet decomposes a signal into localized, finite-length oscillations at different scales. The MODWT variant is particularly useful for time series because it does not decimate the data (no downsampling), meaning the output length matches the input length at every scale.

In practice, the wavelet decomposition separates a series into:

Detail coefficients (D1, D2, D3, …): capturing oscillations at progressively coarser time scales — high-frequency noise in D1-D2, business-cycle frequencies in D3-D4, and longer cycles in higher levels.

Smooth coefficients (S): the low-frequency approximation that captures the trend.

SignalY includes multi-resolution variance analysis, which tells you how much of the total variance is explained at each scale. This is invaluable for understanding whether your series is dominated by high-frequency noise, medium-term fluctuations, or long-run trends.

Empirical Mode Decomposition

filter_emd() implements Empirical Mode Decomposition (Huang et al., 1998), a fundamentally different approach. Where wavelets impose a predetermined basis (Daubechies, Haar, Symmlet, etc.), EMD is fully data-adaptive. It works by iteratively sifting the signal — identifying local extrema, fitting envelopes, and subtracting the mean — until it extracts Intrinsic Mode Functions (IMFs) that satisfy specific oscillatory conditions.

The key advantage of EMD is that it makes no assumptions about stationarity or linearity. The IMFs are defined by the data itself, not by a mathematical basis. This makes EMD particularly powerful for:

Non-stationary signals whose frequency content changes over time.

Non-linear oscillations that cannot be captured by fixed-basis decompositions.

Signals where the “natural” decomposition is not known a priori.

The trade-off is that EMD can be sensitive to end effects and mode mixing, though SignalY’s implementation includes standard mitigations.

HP-GC Bayesian Filter

filter_hpgc() implements the Grant and Chan (2017) unobserved-components Hodrick-Prescott filter, estimated via MCMC. This is a significant upgrade over the traditional HP filter, which requires you to manually set the smoothing parameter λ (the famous λ = 1600 for quarterly data, or λ = 6.25 for annual data, or any of the other arbitrary rules of thumb floating around the literature).

The HP-GC approach formulates the decomposition as a Bayesian unobserved-components model:

A trend component whose second differences are penalized (this is the smoothness prior, equivalent to the HP penalty).

A cycle component modeled as an AR(2) process.

The smoothing parameter λ is estimated from the data via MCMC, not fixed by the user.

This removes one of the most criticized aspects of the classical HP filter — its sensitivity to the arbitrary choice of λ — while preserving its interpretability. The output includes the estimated trend, cycle, and residual, each with full posterior distributions.

filter_all(): Compare All Three

A particularly useful design choice is the filter_all() function, which runs all three decomposition methods on the same series and returns the results in a comparable format. This is not just a convenience function; it is an epistemological statement. No single decomposition method is universally correct. By running all three and comparing, you can identify components that are robust across methods (strong signal) versus components that depend on the specific decomposition assumptions (potentially method artifact).

Pillar 3: How Persistent Is the Signal?

The third question — what is the persistence regime of your series or its components — is critical for downstream modeling. If your extracted trend is a random walk, that has very different implications than if it is a stationary AR process. If your cycle is near-unit-root, standard mean-reversion models will fail.

A Comprehensive Unit Root Battery

test_unit_root() runs four classical tests with complementary null hypotheses:

Test

Null Hypothesis

Key Feature

Augmented Dickey-Fuller (ADF)

Unit root exists

Most widely used; sensitive to lag selection

Phillips-Perron (PP)

Unit root exists

Non-parametric correction for serial correlation

KPSS

Series is stationary

Reversed null; useful as cross-check against ADF

Elliott-Rothenberg-Stock (ERS)

Unit root exists

Point optimal test with higher power near unity

The critical insight is that no single test is definitive. The ADF and PP tests can fail to reject a false unit root (low power near unity). The KPSS test has the opposite null hypothesis, so it can detect stationarity that ADF misses. By running all four and synthesizing the results, SignalY provides a more robust classification than any individual test.

The automated synthesis follows a standard decision logic:

If ADF/PP/ERS reject unit root and KPSS fails to reject stationarity → stationary.

If ADF/PP/ERS fail to reject and KPSS rejects → unit root.

Mixed results → borderline / near-unit-root, flagged for careful interpretation.

This automated synthesis is not a black box; the individual test statistics and p-values are all available for inspection. But the synthesis gives you a quick, defensible classification without manually cross-referencing four separate test outputs.

The Orchestrator: One Call, Full Pipeline

The signal_analysis() function is the centerpiece of SignalY’s design philosophy. A single call can run the complete analysis pipeline:

…and returns a unified result object with print(), summary(), and plot() methods. The plot() method generates interactive plotly dashboards with filter trends, coefficient profiles, PCA loadings, and DFM factor panels.

The formula interface (Y ~ X1 + X2 + X3) makes it feel like a standard R regression call, while the methods argument lets you mix and match analytical layers as needed.

How Well Does It Work?

The Wiki includes recovery benchmarks on synthetic data with known ground truth. These are worth highlighting because they address the most important question: does this actually work?

Task

Method

Recovery Metric

Factor structure (3 latent factors)

PCA / DFM

r > 0.95, exact factor count

Sparse variable selection (5 of 50)

Horseshoe

F1 > 0.85, Precision > 0.90

Logarithmic trend recovery

EMD

r > 0.95 with true trend

Multi-scale cycle extraction

Wavelet (D3+D4)

r > 0.70 with true cycle

Stochastic trend + AR(2) cycle

HP-GC Bayesian

Trend r > 0.90, cycle r > 0.50

Stationarity classification

Unit Root Battery

4/4 correct on synthetic data

A few things stand out:

The Horseshoe achieves over 90% precision in a 5-of-50 sparse selection problem. This means that when it says a variable matters, it is almost always right. The F1 score above 0.85 indicates a good balance between precision and recall.

Factor recovery is near-perfect (r > 0.95), and the DFM correctly identifies the exact number of latent factors.

Wavelet cycle extraction at r > 0.70 and HP-GC cycle extraction at r > 0.50 reflect the inherent difficulty of extracting cyclical components from noisy data. These are realistic numbers, not inflated claims.

Unit root classification achieves 100% accuracy on synthetic data with clear-cut cases. Real-world data is messier, but this validates the synthesis logic.

Who Should Use SignalY?

SignalY is built for three overlapping communities:

Economists and econometricians working with panel or multivariate time series data who need to move from raw data to structural inference — identifying relevant variables, extracting latent factors, decomposing signals, and characterizing persistence — without stitching together five different packages.

Quantitative researchers in finance, macro, or political economy who face high-dimensional predictor sets and need principled Bayesian variable selection rather than stepwise regression or arbitrary LASSO tuning.

Data scientists working on signal processing problems where the signals are non-stationary, non-linear, or embedded in high-dimensional panels, and where the standard Python signal processing toolkit does not provide the statistical rigor needed for publication-quality inference.

Getting Started

Installation is straightforward:

# From GitHub

remotes::install_github("IsadoreNabi/SignalY")

library(SignalY)

# Minimal workflow

data<-data.frame(Y=as.vector(Y), X)

result<-signal_analysis(data=data, y_formula="Y",

methods=c("pca", "wavelet", "unitroot"))

plot(result)

The package is MIT-licensed, actively maintained (current version 1.1.2), and designed to work with standard R data frames.

The Bigger Picture

What makes SignalY interesting is not any single method — the Horseshoe prior, MODWT, EMD, and unit root tests all exist in other packages. The value is in the integration. By placing Bayesian sparse regression, spectral decomposition, and persistence analysis inside a single coherent framework with a unified interface, SignalY enables workflows that are difficult to replicate otherwise:

Run a Horseshoe regression to select variables, then decompose the fitted signal with wavelets, then test the stationarity of the extracted components — all without changing packages, data formats, or mental models.

Compare wavelet, EMD, and HP-GC decompositions of the same series to identify robust components versus method-dependent artifacts.

Use the DFM to discover latent factors, then test each factor’s persistence regime to inform your downstream modeling choices.

In applied econometrics, the quality of your inference depends on the coherence of your pipeline. SignalY makes that coherence a feature rather than a chore.

SignalY is developed by José Mauricio Gómez Julián. The source code, documentation, and wiki are available at github.com/IsadoreNabi/SignalY under the MIT License.

You can also find this library at CRAN and download it directly from R and RStudio.

LISTEN TO THIS POST AS A PODCAST:

Imagine you’re monitoring a manufacturing line, and the sensor readings suddenly look… different. The numbers aren’t obviously wrong — they’re within range — but something has shifted. Or picture an economist staring at decades of GDP data, trying to pinpoint exactly when a country’s growth model fundamentally changed. Or a doctor watching a patient’s vitals, waiting for the moment “stable” tips into “critical.”

All of these scenarios share the same underlying question: when did the system switch from one regime to another?

This is the problem of regime change detection (also called changepoint detection), and it’s one of the most practically important — and theoretically rich — problems in time series analysis. A new open-source R package called RegimeChange tackles this problem with unusual breadth, combining classical statistics, Bayesian inference, and even deep learning under a single, coherent interface. In this post, I’ll walk you through what it does, how it works, and why it matters — in plain language, without cutting corners on the technical details.

The Problem: Signal vs. Noise

Every observable system fluctuates. The central question of changepoint detection is deceptively simple: is this fluctuation just noise (random variation within the same regime), or is it signal (evidence that the system has transitioned to a qualitatively different state)?

This is harder than it sounds. There’s an irreducible tension between two types of error:

False alarm (Type I): You detect a change where none exists. In manufacturing, this means shutting down a line for no reason. In medicine, it’s a false positive that triggers unnecessary intervention.

Missed detection (Type II): You fail to detect a real change. In finance, this means holding a position through a regime shift. In epidemiology, it means missing the start of an outbreak.

Every detection algorithm negotiates this trade-off through its threshold: how much evidence do you demand before declaring that the world has changed? Set it too low and you cry wolf; set it too high and you react too late. There is no universal answer — the right threshold depends on the relative cost of each type of error in your specific context.

What Makes RegimeChange Different

Several R packages already address changepoint detection — the venerable changepoint package, wbs, not, ecp, and the Python ruptures library, to name a few. Each has strengths and limitations. RegimeChange distinguishes itself by integrating approaches that are usually siloed:

Frequentist and Bayesian methods together. Most packages pick one paradigm. RegimeChange gives you both, plus deep learning, all callable through the same detect_regimes() function.

Offline and online modes. You can analyze a complete dataset retrospectively (“when did the changes occur?”) or process streaming data in real time (“is a change happening right now?”) using the same library.

Native uncertainty quantification. Every changepoint estimate comes with confidence intervals (via bootstrap for frequentist methods) or full posterior distributions (for Bayesian methods). This isn’t just a point estimate — it’s a statement about how confident you should be.

Robustness to messy data. Real-world data has outliers, heavy tails, and autocorrelation. RegimeChange includes configurable robust estimation and AR(1) pre-whitening — features that, as the benchmarks show, make a dramatic difference on contaminated data.

An optional Julia backend. For large datasets, the package can transparently dispatch to high-performance Julia implementations while keeping the R interface you’re used to.

Let’s look at each of these in more detail.

The Three Method Families

RegimeChange organizes its detection algorithms into three families. Here’s what each one does, explained simply.

Frequentist Methods

These are the classical, well-established workhorses of changepoint detection.

CUSUM (Cumulative Sum) is the granddaddy of them all, dating to E. S. Page’s 1954 paper. The idea is beautifully intuitive: you accumulate deviations from a target (or “baseline”) value over time. If the system is in the same regime, positive and negative deviations cancel out, and the cumulative sum hovers near zero. When a change occurs, deviations start piling up in one direction, and the statistic grows. When it crosses a threshold, you sound the alarm. CUSUM runs in O(n) time and is ideal for detecting a single change in mean, especially in online monitoring scenarios.

PELT (Pruned Exact Linear Time), introduced by Killick, Fearnhead, and Eckley in 2012, is the modern gold standard for detecting multiple changepoints. It uses dynamic programming to find the globally optimal segmentation of your data — the set of changepoints that minimizes a cost function (essentially: how well do the segments fit the data, penalized by the number of segments). The “pruning” part is clever: it discards candidate changepoint locations that provably can’t be optimal, which brings the average-case complexity down from O(n²) to O(n). RegimeChange supports several penalty criteria — BIC, AIC, MBIC, MDL — or you can specify a manual numeric penalty.

Binary Segmentation is a simpler, greedy alternative: find the single best changepoint, split the data there, then recurse on each segment. It’s fast (O(n log n)) but doesn’t guarantee the global optimum. Wild Binary Segmentation (WBS), from Fryzlewicz (2014), improves on this by searching over many random sub-intervals rather than the full dataset, making it much more robust when changepoints are close together.

The package also includes FPOP (Functional Pruning Optimal Partitioning), which maintains piecewise-quadratic cost functions for even better theoretical guarantees; E-Divisive, a nonparametric method using energy statistics that can detect changes in any aspect of the distribution; Kernel-based CPD, which maps data into a reproducing kernel Hilbert space to capture complex distributional shifts; and NOT (Narrowest-Over-Threshold), which excels at precise localization.

Bayesian Methods

Where frequentist methods give you a point estimate and (if you ask) a confidence interval, Bayesian methods give you something richer: a full probability distribution over when the change might have occurred.

BOCPD (Bayesian Online Changepoint Detection), from Adams and MacKay (2007), is the flagship. At each time step, it maintains a posterior distribution over the “run length” — the number of observations since the last changepoint. When a new data point arrives, it updates this distribution: either the run length grows by one (no change), or it resets to zero (change detected). The probability of a reset at each step is governed by a “hazard function,” typically a geometric distribution representing a constant probability of change per time step.

What makes BOCPD powerful is that it naturally produces, at every time point, the probability that a changepoint just occurred. This is a fundamentally different kind of output than a binary “change/no-change” flag — it’s a calibrated measure of confidence that updates with every new observation. RegimeChange implements BOCPD with several conjugate prior models: Normal-Gamma (for unknown mean and variance), Normal with known variance, Gamma-Poisson (for count data), and Normal-Wishart (for multivariate data).

Shiryaev-Roberts is another Bayesian sequential method, based on work by Shiryaev from the 1960s. It accumulates likelihood ratios from all possible past changepoint times and is asymptotically optimal for minimizing detection delay — that is, for detecting changes as quickly as possible once they occur.

Deep Learning Methods

For complex, nonlinear patterns that classical methods struggle with, RegimeChange offers optional deep learning detectors (requiring keras and tensorflow):

Autoencoders are trained to reconstruct “normal” patterns. When the data changes regime, reconstruction error spikes — the model can’t rebuild what it hasn’t seen before.

Temporal Convolutional Networks (TCNs) use dilated causal convolutions to model long-range temporal dependencies, operating either in supervised mode (if you have labeled changepoints for training) or unsupervised mode (predicting the next value and flagging prediction errors).

Transformers bring self-attention to the problem, capturing long-range relationships in the time series.

Contrastive Predictive Coding (CPC) learns representations through self-supervised contrastive learning, detecting changes where learned embeddings shift significantly.

An ensemble mode combines multiple deep learning methods, requiring a minimum number of them to agree before declaring a changepoint — a strategy that trades some sensitivity for robustness.

One Interface to Rule Them All

The genius of RegimeChange is that you don’t need to learn a different API for each method. Everything flows through a single function:

library(RegimeChange)

# Generate data with a changepoint at t=200

set.seed(42)

data<-c(rnorm(200, 0, 1), rnorm(200, 2, 1))

# Detect using PELT (the default offline method)

result<-detect_regimes(data, method="pelt")

print(result)

plot(result)

# Switch to Bayesian online detection

result<-detect_regimes(data, method="bocpd",

prior=normal_gamma(mu0=0, kappa0=1,

alpha0=1, beta0=1))

# Use CUSUM for online monitoring

result<-detect_regimes(data, method="cusum",

mode="online", threshold=5)

You specify what kind of change you’re looking for (type = "mean", "variance", "both", "trend", or "distribution"), how many changes you expect ("single", "multiple", or a specific integer), and the penalty criterion for model complexity. The function returns a regime_result object containing the detected changepoints, their confidence intervals, segment-by-segment statistics (mean, variance, etc.), and — for Bayesian methods — the full posterior distribution.

Online Detection

For real-time monitoring, you create a persistent detector object and feed it data one observation at a time:

detector<-regime_detector(method="bocpd",

prior=normal_gamma(),

threshold=0.5)

for (xindata_stream) {

detector<-update(detector, x)

if (detector$last_result$alarm) {

message("Changepoint detected at time ", detector$last_result$t)

detector<-reset(detector)

}

}

This is the pattern you’d use for industrial monitoring, fraud detection, or epidemiological surveillance — anywhere data arrives sequentially and you need to react in real time.

Robustness: Where RegimeChange Really Shines

Real data is messy. It has outliers, heavy tails, and autocorrelation. Standard changepoint methods, which typically assume independent, normally distributed observations, can fail dramatically under these conditions.

RegimeChange addresses this with a configurable robustness layer in its PELT implementation. When you set robust = TRUE, the package:

Winsorizes the data (clips extreme values beyond a specified quantile) to limit the influence of outliers.

Uses Huber M-estimation or Tukey biweight loss functions instead of standard squared-error loss. These functions grow linearly (Huber) or flatten out entirely (Tukey) for large residuals, so a single outlier can’t dominate the cost calculation.

Employs the Qn scale estimator (from Rousseeuw and Croux, 1993), which is far more efficient than the median absolute deviation (MAD) — 82% efficiency vs. 37% — while maintaining the same 50% breakdown point (meaning up to half the data can be contaminated before the estimator breaks).

You can also set robust = "auto", which analyzes the data’s contamination level — comparing the MAD to the standard deviation and counting outlier proportions — and automatically selects the appropriate robustness level ("none", "mild", "moderate", or "aggressive").

For autocorrelated data, the correct_ar = TRUE option estimates the AR(1) coefficient and applies a pre-whitening transformation (subtracting the lagged value scaled by the autocorrelation coefficient) before running detection. This prevents autocorrelation from inflating false positive rates.

The Benchmark Numbers

The package’s wiki reports extensive benchmarks against established R packages (changepoint, wbs, not, ecp) across 17 scenarios with 50 replications each. The results are striking:

Overall: RegimeChange’s automatic selector achieved the highest mean F1 score (0.804) across all methods tested.

Contaminated data: The robust mode achieved F1 = 0.998 across all contamination scenarios, versus 0.479 for the standard changepoint PELT — a 108% improvement on messy data.

Subtle variance changes (2:1 ratio): RegimeChange scored 0.667 vs. 0.400 for reference packages — a 67% improvement.

Strong autocorrelation (AR coefficient 0.7): RegimeChange scored 0.900 vs. 0.720 — a 25% improvement.

In 16 of 17 scenarios, RegimeChange either won or tied. The single loss was marginal (0.017 in one heavy-tailed scenario).

Uncertainty Quantification: Beyond Point Estimates

A changepoint location of “observation 200” is only half the story. The other half is: how confident are we? RegimeChange takes this seriously, providing two types of uncertainty:

Location uncertainty — how precise is the estimate? For frequentist methods, the package uses block bootstrap resampling: it repeatedly resamples blocks of the data (preserving local dependence structure), reruns detection, and computes 95% confidence intervals from the distribution of bootstrap estimates. For Bayesian methods, uncertainty comes naturally from the posterior distribution over run lengths.

Existence uncertainty — is there even a change at all? BOCPD produces, at each time point, the posterior probability that a changepoint just occurred. This is arguably more informative than a p-value: it’s a direct probabilistic statement that you can use for decision-making.

The Julia Backend

R is wonderful for data analysis, but it can be slow for computationally intensive tasks. RegimeChange ships with an optional Julia backend — a complete reimplementation of the core algorithms (PELT, FPOP, BOCPD, CUSUM, Kernel CPD, WBS, and multivariate PELT) in Julia, a language designed for numerical performance.

The integration is seamless. You initialize Julia once:

init_julia()

julia_available() # Returns TRUE if ready

After that, the package automatically dispatches to Julia for large datasets (n > 1000 by default) while using R for smaller ones. You can benchmark the difference with benchmark_backends(). The Julia implementation includes thoughtful numerical engineering: Welford’s algorithm for numerically stable running mean/variance, Kahan compensated summation for cumulative sums, log-domain computations to avoid underflow in BOCPD, and careful handling of ill-conditioned covariance matrices in the multivariate case.

If Julia isn’t installed, the package simply falls back to the R implementation — no errors, no fuss.

Evaluation and Comparison

RegimeChange includes a comprehensive evaluation framework. If you know the true changepoints (e.g., in simulated data or a well-studied real dataset), you can compute a full battery of metrics:

This gives you precision, recall, and F1 score (with a tolerance window for matching), Hausdorff distance (the worst-case localization error), Rand Index and Adjusted Rand Index (segmentation agreement), and the covering metric (a weighted IoU measure). You can also run compare_methods() to test multiple algorithms on the same data and see the results side by side.

The package ships with several built-in datasets: well_log (geophysical measurements), industrial_sensor data, economic_cycles, and simulated_changepoints — giving you realistic examples to experiment with.

When to Use What

Here’s a practical guide based on the library’s design and benchmark results:

Your Situation

Recommendation

Clean data, clear mean shifts

PELT with default settings

Outliers or heavy tails

PELT with robust = TRUE (or "auto")

Autocorrelated time series

PELT with correct_ar = TRUE

Need real-time detection

BOCPD or CUSUM via regime_detector()

Need probability of change (not just yes/no)

BOCPD

Nonparametric, no distributional assumptions

E-Divisive or Kernel CPD

Complex nonlinear patterns (and you have data to train on)

Deep learning methods

High-dimensional multivariate data

Sparse Projection CPD

Not sure which method to use

Ensemble mode, or let method = "auto" choose

The Bigger Picture

What I find compelling about RegimeChange is its philosophical stance. The wiki frames changepoint detection not just as a technical problem but as an epistemological one: how do we distinguish real change from noise? The likelihood ratio — the ratio of how probable an observation is under the “changed” hypothesis vs. the “unchanged” hypothesis — is literally a quantification of surprise. Each observation casts a vote, evidence accumulates, and the decision threshold represents how much surprise we demand before acting.

This framing connects the technical machinery to the real-world stakes. Whether you’re monitoring a factory, tracking a disease outbreak, or studying climate data, the fundamental structure is the same: the world was in one state, it transitioned to another, and you need to detect that transition as reliably and quickly as possible.

RegimeChange gives you a unified toolkit for that task — one that spans the classical-to-modern spectrum, handles messy data gracefully, tells you not just where the change is but how confident you should be, and scales from your laptop to a Julia-accelerated backend when you need speed.

Getting Started

RegimeChange is available on GitHub and installs like any R package from source:

It requires R ≥ 4.0.0 and depends on ggplot2, rlang, cli, and magrittr. The Julia backend is optional (requires Julia ≥ 1.6 and the JuliaCall R package), as are the deep learning methods (require keras and tensorflow). The package ships with three vignettes — an introduction, an offline detection guide, and a Bayesian methods tutorial — and the wiki is a comprehensive reference covering everything from mathematical foundations to detailed benchmarks.

For researchers and practitioners who need rigorous, flexible, and robust changepoint detection in R, RegimeChange is well worth a close look.

You can also find this libraryat CRAN and download it directly from R and RStudio.

LISTEN TO THIS POST AS A PODCAST:

You have a national Consumer Price Index. It is a single number per year. What you actually want is the price index for each sector of the economy — manufacturing, services, agriculture, construction — because those individual paths are what your model, your policy analysis, or your investment thesis really needs. You know how the sectors combine into the whole: the weights are public, or at least knowable. What you do not know is the sectoral numbers themselves. You only ever see their weighted sum.

This is the disaggregation problem. It sounds like bookkeeping. It is actually a quietly profound statistical question, and the R package BayesianDisaggregation — built by José Mauricio Gómez Julián — tackles it with a degree of intellectual honesty that is rare in software. This post is a deep, plain-language tour of what the package does, why it works the way it does, and what it teaches about building statistical tools that tell the truth.

If you want to follow along with the code, the project’s wiki has installation instructions, function references, and worked examples. This post deliberately stays code-free so the ideas come through.

The problem, precisely

Let’s make it concrete. You observe an aggregate index — call it the CPI — over T years. You also have a matrix of weights W: for each year and each of K sectors, W tells you that sector’s share of the total. The weights sum to one within each year. The aggregate is, up to measurement noise, the weighted sum of the latent sectoral indices:

CPI at year t ≈ the weighted sum of the K sectoral indices, using that year’s weights.

The goal: recover the K sectoral indices — call them φ — from the single aggregate series and the known weights.

Here is the catch, and it is the entire heart of the matter. At every single year, the aggregate pins down one linear combination of the K sectors. The remaining K−1 directions are completely unconstrained by the data. With four sectors, you have one equation and four unknowns per year. The system is, in a precise mathematical sense, under-determined.

This is not a numerical annoyance you can engineer away. It is structural. Any method that hands you a single, sharp sectoral path from an aggregate alone is, whether it admits it or not, smuggling in assumptions to fill the gap — and most methods do not tell you how much of the answer is data and how much is assumption.

The question is not can you disaggregate. You always can. The question is: can you do it honestly, showing your work, and carrying the right amount of uncertainty forward?

The wrong way: a cautionary tale

The first version of the package — the 0.1.x line — advertised “MCMC-free Bayesian disaggregation.” The pitch was appealing: no slow Markov chain Monte Carlo sampling, just clean closed-form math. The implementation used a family of deterministic update rules — weighted, multiplicative, Dirichlet, adaptive — over the prior weight matrix.

It did not work. Not in the sense of crashing. In the much more dangerous sense of appearing to work while silently not doing the one thing it claimed to do.

The package’s own author, in a moment of radical honesty that is worth pausing on, audited the 0.1.x family and catalogued six foundational defects, labeled F1 through F6:

F1 — the aggregate never entered the computation. The “posterior” was derived entirely from the prior weight matrix. The actual observed CPI — the one piece of real evidence — was never used. The method was not conditioning on data; it was rearranging priors.

F2 — the Dirichlet concentration cancelled on renormalization. A parameter that was supposed to control how concentrated the sectoral estimates were simply vanished in the algebra when weights were normalized to sum to one.

F3 — the temporal pattern cancelled too. A component meant to encode smoothness over time also disappeared in the renormalization.

F4 — the “efficiency” term was a fixed constant. It looked like a data-dependent quality score; it was actually invariant.

F5 — there were no recovery tests. No one had ever generated synthetic data with a known truth and checked whether the method got it back.

F6 — a correlation helper cheated. It computed both Pearson and Spearman correlation and reported whichever was larger, a form of silent data-snooping.

The most damning of these is F1. A Bayesian method that does not condition on data is not a Bayesian method. It is a deterministic transformation dressed in Bayesian vocabulary. And the worst part is that it looked reasonable — it returned numbers, they moved in plausible directions, and nothing crashed.

The author’s response is, I think, the most important thing about this whole project. Rather than patching the defects one by one — adding the CPI here, fixing the concentration there — the author recognized that the foundational problem (not using the data) cannot be fixed within a deterministic re-weighting framework. The fix is not a patch. The fix is a fundamentally different model: one in which the aggregate enters as genuine evidence.

So the entire 0.1.x family was deleted. Every function — bayesian_disaggregate(), compute_L_from_P(), spread_likelihood(), the four update rules, the grid search, the save function, the cheating correlation helper — all of it, gone. In its place: two Bayesian engines that actually condition on the data. The package version jumped to 0.2.0, the DESCRIPTION was edited to remove any claim of novelty, and the documentation was rewritten to be explicit about what was removed and why.

This is what intellectual honesty in software looks like. It is not common. We should notice it when it happens.

The right idea: the aggregate as evidence

The conceptual move is simple to state and deep in consequence. Instead of treating the relationship between the aggregate and the sectors as a renormalization identity — a bit of algebra you apply after the fact — treat it as an observation density. The aggregate CPI is data. It is evidence about the latent sectors. The model should condition on it.

In the package’s canonical engine, this means: the latent sectoral indices φ evolve over time as a random walk with drift, and the observed CPI is generated from the weighted sum of the sectors with some observation noise. The aggregate is not a constraint imposed after estimation; it is the likelihood. The sectors come out the other side as a posterior distribution — not a single number, but a full cloud of plausible values with credible intervals.

This is the difference between solving an equation and updating beliefs in light of evidence. The first gives you a point. The second gives you a distribution. And as we will see, the distribution is the whole point.

Two engines, one trade-off

The package offers two ways to do the Bayesian inference, and the choice between them is a clean, well-explained trade-off between richness and exactness.

The state-space MCMC engine

This is the canonical, full-featured model. The sectoral indices live in log space, which guarantees they stay positive — a natural constraint for price indices that a model in raw levels could violate. Each sector’s log-index follows a random walk with its own drift and its own innovation scale (the amount of jitter per period).

Two layers of hierarchical structure make this more than K independent random walks:

Partial pooling on the drift. Each sector has its own drift, but the drifts are drawn from a common distribution. This means sectors share information about their average growth rate without being forced to be identical — the classic shrinkage trade-off.

Partial pooling on the innovation scale. Similarly, each sector’s volatility is drawn from a shared distribution. Sectors borrow strength in estimating how jittery they are.

The initial cross-section — the starting levels of the sectors at the first period — is anchored at the aggregate level with an estimable dispersion parameter. This is a subtle but important point. In the old, broken 0.1.x family, the “concentration” parameter was supposed to control how spread out the sectors were, but it cancelled in the algebra and had no effect. In the new model, the dispersion is a genuine parameter that the data and priors can actually estimate. It does not cancel. It does real work.

Finally, the observation: the CPI is modeled as coming from a Student-t distribution centered at the weighted sum of the sectors, with an estimable scale. The Student-t (rather than a Gaussian) makes the model robust to outliers in the aggregate — a heavy-tailed observation can be accommodated without wrecking the fit. If you prefer, you can switch to a plain Gaussian observation.

Because this model is not conjugate — the log transform, the Student-t, and the hierarchical structure break the neat algebra that would allow a closed-form solution — it is fit by Hamiltonian Monte Carlo via Stan (using either the cmdstanr or rstan backend). HMC is the gold standard for this kind of model: it handles the correlated, high-dimensional parameter space efficiently and comes with reliable diagnostics. The package runs four chains by default, checks the R-hat convergence statistic and the number of divergent transitions, and returns posterior draws of every sectoral index at every period.

The closed-form conjugate engine

The second engine is the linear-Gaussian counterpart. The sectoral indices evolve as a random walk in levels (not logs), and the aggregate is observed with Gaussian noise. This model is conjugate, which means its exact posterior can be computed in closed form — no MCMC, no sampling, no convergence diagnostics. The tool is the Kalman filter combined with the Rauch-Tung-Striebel smoother: the filter passes forward through time, updating beliefs about the sectors given each new CPI observation, and the smoother passes backward, refining those beliefs using future information.

If you want joint posterior draws — not just the smoothed means and variances, but actual correlated samples from the full posterior — the package uses the Durbin-Koopman simulation smoother, a elegant technique that produces draws with the correct cross-time and cross-sector covariance structure. These draws are not marginal approximations; they are genuine samples from the joint posterior.

This engine is the “correct realization of the original MCMC-free posterior idea.” The 0.1.x family wanted a closed-form Bayesian answer; the problem was not that closed-form is un-Bayesian (conjugacy is perfectly Bayesian), but that the old method did not use the data. This engine uses the data — the aggregate enters as the observation equation — and it does so in exact, closed form.

The trade-off is explicit and documented. The closed-form engine buys you speed and mathematical exactness. It costs you three things: positivity (levels can drift slightly negative, which logs prevent), robustness (Gaussian observations are sensitive to outliers, which the Student-t handles), and the cross-sector hierarchy (there is no partial pooling in the linear-Gaussian model). The MCMC engine buys you all three of those, at the cost of sampling.

Both engines return the same thing: an array of posterior draws of the sectoral indices, with dimensions [periods × sectors × draws], plus summary tables of medians and 95% credible bands.

The honesty at the center: weak identification

Here is where the package earns its deepest respect. It would be tempting, after building a real Bayesian model that conditions on the data, to declare victory and hand users sharp sectoral estimates. The package does not do this. Instead, it is explicit about a fact that most disaggregation methods gloss over: the sectoral split is only weakly identified.

Remember the under-determination: at each period, the aggregate pins down one linear combination of the K sectors. The remaining K−1 directions are governed by the prior — the cross-sectional dispersion and the temporal smoothness — not by the data. This means the posterior intervals for individual sectors are wide, and they are influenced by the prior. This is not a bug. It is not a limitation to be engineered away. It is the correct representation of what the data can and cannot tell you.

The package’s own recovery tests — which generate synthetic data from the model’s own data-generating process, where the true sectoral paths are known — confirm this directly. The aggregate is recovered essentially perfectly: the correlation between the fitted aggregate and the true aggregate is above 0.95, often essentially 1.0. The aggregate is strongly identified. But the sectoral coverage — the fraction of times the true sectoral path falls within the 95% credible band — is around 0.84, with the bands being deliberately wide. The test asserts that coverage exceeds 0.70, a conservative threshold, because the package refuses to claim sectoral precision that the data cannot deliver.

This is “rigour by layers”: assert tightly what is identified, assert conservatively what is not. It would be easy to tune the prior to produce narrower, more impressive-looking bands. The package deliberately does not.

Why the full posterior matters: propagating uncertainty

If the sectoral estimates are uncertain — wide bands, prior-influenced — then what good are they? This is where the design of the package reveals its purpose. The sectoral indices are not the final product. They are input to a downstream model. In the author’s research program, they feed a nested Ornstein-Uhlenbeck model of price gravitation. But the principle is general: any time a disaggregated estimate feeds a second-stage analysis, the uncertainty in the first stage should flow into the second.

The package handles this by multiple imputation, following Rubin’s rules. Each posterior draw of the sectoral indices is treated as one imputation — one plausible version of the truth. The downstream model is fit once per imputation, and the results are combined. The effect is that the weak per-sector identification — the wide bands, the prior influence — is carried forward into the downstream uncertainty intervals rather than being discarded. You do not plug in a point estimate and pretend it is the truth. You plug in the whole cloud and let the cloud’s shape propagate.

The package’s documentation is candid about a consequence: because disaggregation is under-determined, the random-walk smoother prior dilutes the reversion signal, biasing the downstream reversion speed toward slowness by a modest, quantified amount (roughly 13–26%). Crucially, the direction is conservative — the true gravitation is at least as fast as reported — and the fraction of missing information that is propagated is about 0.4. This is not hidden. It is measured, reported, and flagged as a property of honest under-determination.

A sharp contrast: an ad-hoc method that simply added noise to a point estimate did not produce proper imputations and gave sub-nominal coverage when routed through Rubin’s rules. The coherent posterior from the conjugate engine — the one that actually conditions on the data — did. The mathematics of multiple imputation demands proper posterior draws; garbage in, garbage out.

How it is validated

The package’s validation strategy is worth studying because it embodies a philosophy: test the identified quantity tightly, test the unidentified quantity conservatively, and test the computation itself exactly.

Three layers, kept deliberately separate:

Smoke tests run always, on every check. They confirm that both engines compile, sample, and return the correct [periods × sectors × draws] array structure on synthetic data. They catch breakage.

Recovery tests are gated behind an environment flag because they require actually compiling and sampling the Stan model, which is slow. They generate data from the model’s own data-generating process — the same random walk with drift, the same partial pooling, the same aggregate observation — so the true sectoral paths are known. Then they check: does the aggregate come back essentially perfectly? (Yes, correlation above 0.95.) Do the sectoral bands cover the truth at a reasonable rate? (Yes, above 0.70, honestly wide.) The recovery test is well-posed because the simulator uses the same process as the model. If the model cannot recover its own data, something is wrong with the sampler or the implementation. If it can, you have a meaningful baseline.

Golden tests run always and are the most stringent. They use Stan’s generate_quantities function — which deterministically recomputes derived quantities from frozen parameter draws, with no random number generation involved — and demand a bit-for-bit match against a frozen reference output. This catches any change to the model’s computed quantities: if someone edits the Stan code and the log-likelihood values shift by even one bit, the test fails. The reference fixture is generated by the same code path, isolating the CSV serialization so the comparison is exact.

This is not the “does it run?” school of testing. It is the “does it compute the right thing, and does it compute exactly the same thing tomorrow?” school.

Where it sits among existing methods

The package is careful — almost unusually careful — about situating itself relative to the existing literature. It makes no claim of being the first or only solution to this problem. The documentation uses the phrase “we did not find” rather than “we are the first,” and the DESCRIPTION file was explicitly edited to remove any “novel/original” claim.

The adjacent traditions, and what each misses:

Biproportional balancing (RAS, IPF) iteratively scales a matrix to match new margins. It is deterministic: no posterior, no credible intervals, no treatment of the aggregate as evidence. It is a useful accounting tool, not an inference method.

Temporal disaggregation (Denton, Chow-Lin, Fernández) distributes a low-frequency aggregate to higher frequency using an indicator series. This is a temporal problem — splitting annual into quarterly — not a cross-sectional one. It assumes you already have the sectoral decomposition and just need finer time resolution.

Forecast reconciliation (MinT and related methods) projects inconsistent hierarchical forecasts onto a coherent subspace. It is forecast-centric and linear-algebraic: it corrects forecasts that do not add up, rather than recovering latent components from an aggregate by Bayesian updating.

Compositional or Dirichlet state-space models evolve simplex weights over time. They model how shares move, not how the components themselves are recovered conditioned on their weighted sum.

Each tradition addresses a real problem. None, as far as the package’s author could find, does exactly this: recover latent cross-sectional components from a single aggregate by conditioning on it as a genuine observation density and returning a posterior that can be propagated downstream. The claim is narrow and checkable, not sweeping.

The data pipeline

The package is not just a model; it is a usable tool. It includes hardened readers for the real inputs. A CPI reader pattern-matches on column headers (in English or Spanish — it recognizes “date,” “fecha,” “year,” “año” for the time column and “cpi,” “indice,” “price” for the value column), parses localized number formats (European-style decimals and thousands separators), collapses duplicate years by averaging, and returns a clean, sorted data frame. A weights reader loads a sector-by-year table, normalizes weights to the simplex within each year, and handles missing entries gracefully.

An alignment function intersects the years covered by the CPI and the weights, ensuring both cover the same periods before either engine runs. A convenience wrapper reads both files and runs the disaggregation in one call. And a simulator generates synthetic data from the model’s own data-generating process — the same random walk with drift, the same partial pooling, the same aggregate observation — so that recovery tests, examples, and exploratory analysis are always well-posed.

One data note worth flagging, because it is a common error: the model works in index levels, not rates of change. Feeding a percent-change series (inflation rate) instead of a level series (the CPI itself) is a category error — the aggregate would not be on the same scale as the weighted sum of the sectors. The CPI must be a level series, re-indexed to the same base as whatever the sectors will be compared against.

The bigger lesson

You could read this package as a technical contribution: a Bayesian state-space model for disaggregation with two engines, honest uncertainty, and a propagation contract. That reading is correct but incomplete.

The deeper lesson is about how to build statistical software that tells the truth. The 0.1.x family did not fail by crashing. It failed by producing plausible-looking output that did not depend on the data. That is the most dangerous failure mode in statistics, because there is no error message. The numbers look reasonable. The plots look smooth. Nothing warns you that the entire computation is a rearrangement of priors.

The author caught it — caught it in their own work, which is harder than catching it in someone else’s — by doing the unglamorous thing: generating data with a known truth and checking whether the method recovered it. When it did not, they did not patch. They deleted and rebuilt. And then they documented the deletion, in public, with the defects labeled and explained, so that anyone reading the history would understand not just what changed but why.

The resulting package has a quality that is hard to name but easy to feel when you read the source: every design choice has a reason, every reason is documented, and the documentation is honest about what the method can and cannot do. The aggregate is strongly identified; the sectors are weakly identified; the uncertainty is wide and prior-influenced; and all of that is surfaced, not hidden, because the whole point is to carry that uncertainty forward rather than fake it away.

In a field where it is tempting to claim sharp results from sparse data, this is a quiet act of integrity. The package does not solve the under-determination. Nothing can. It does something better: it honors it, by returning the wide, honest, propagatable posterior that the data actually supports.

The package, its source code, installation instructions, and full function reference are on GitHub, with extended documentation in the wiki. It is MIT-licensed and written in R, with the MCMC engine powered by Stan.

You can also find this libraryat CRAN and download it directly from R and RStudio.

LISTEN TO THIS POST AS A PODCAST:

When Market Prices Gravitate: A Bayesian Look at an Old Question in Economics

An old question, asked again — properly

There is a question in economics that is older than most of the academic disciplines that border it. Do market prices — the noisy, day-to-day, here-and-now prices at which goods actually change hands — tend to settle toward some underlying center of gravity? And if they do, how fast, how violently, and through what mechanism?

Classical political economy, from Smith and Ricardo through Marx, thought they do. The idea was that behind the churning surface of market prices there sit “prices of production”: long-run, cost-anchored prices toward which actual prices are pulled, the way a spring pulls a weight back toward its rest position. In the Marxian version, there is one more layer underneath: those prices of production themselves are supposed to gravitate around “values,” the labour embodied in commodities. Whether any of this is true is an empirical question, and for a long time the empirical tools to answer it were not really up to the job.

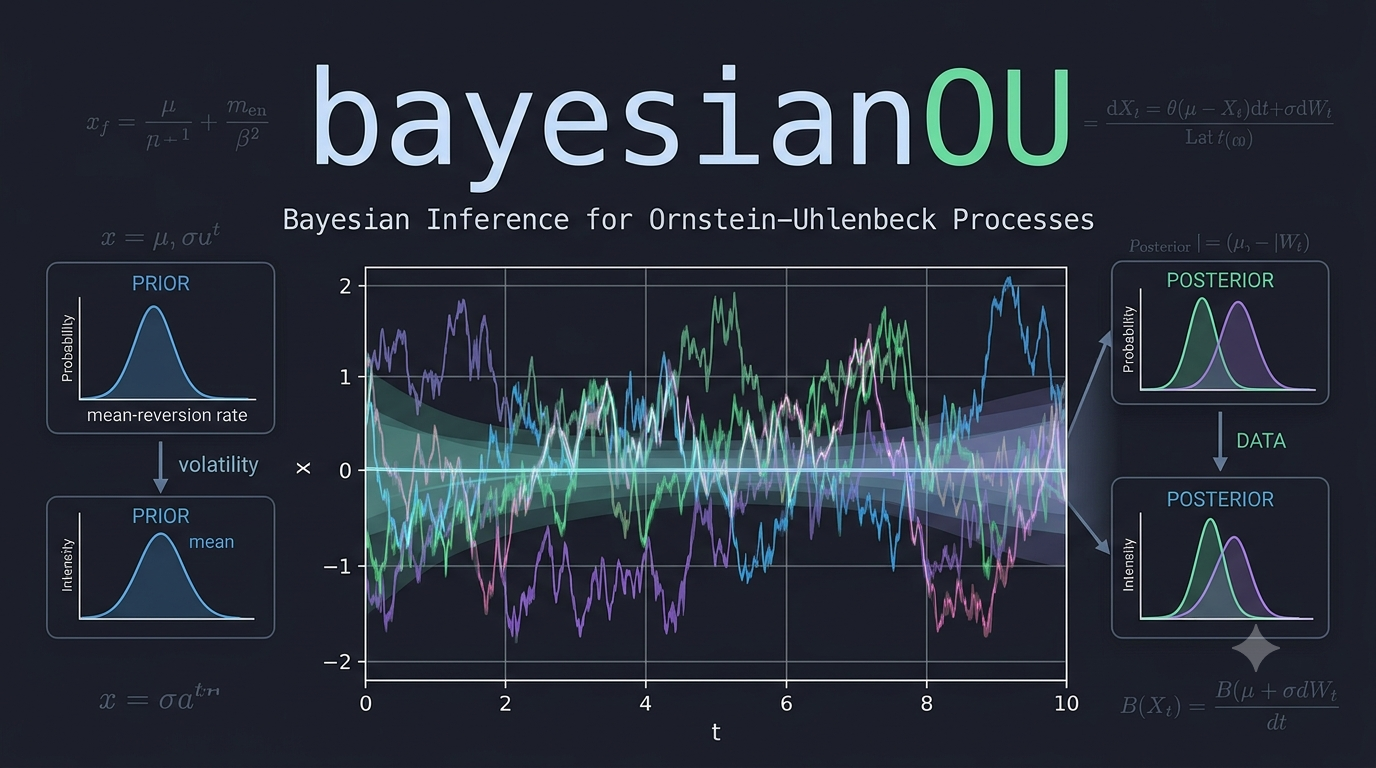

A small R package called bayesianOU, written by José Mauricio Gómez Julián and hosted on GitHub, takes a serious swing at that question. It is not the first attempt to test price gravitation statistically, but it is one of the most technically careful I have seen, and it is built in a way that is instructive far beyond the Marxian debate that motivates it. What follows is a walkthrough of what the package does, why it is interesting, and — just as importantly — where it honestly admits its own limits.

The tool that makes it possible: the Ornstein-Uhlenbeck process

Strip the economics away for a moment and the statistical core of the package is a workhorse object from physics: the Ornstein-Uhlenbeck (OU) process. Imagine a particle moving in a fluid, attached to a spring. Brownian motion jiggles it randomly; the spring pulls it back toward a fixed point. The further it drifts away, the harder the pull. The result is a wiggly series that never settles but always tends to settle — a mean-reverting random walk.

The OU process is exactly the mathematical object you want when you suspect a variable is noisy but anchored. It has a “speed of reversion” (how hard the spring pulls) and an “equilibrium level” (where the spring’s rest point is). Estimate those, and you can say something quantitative about gravitation: not just “yes, prices come back,” but “they come back with a half-life of about nine years.”

That number — the half-life — is the prize. It is the difference between “market prices eventually settle” (which could mean anything) and “market prices settle on a timescale comparable to a business cycle” (which is a falsifiable, interpretable claim).

What the package actually builds

The package fits, by Bayesian inference, a family of models built on the OU process but considerably richer than the textbook version. There are two first-class models, sharing one inference engine.

The single-level model

The first model asks: do market prices revert toward an equilibrium that is a function of the prices of production, and what does that reversion look like once we let it be nonlinear, volatile, heavy-tailed, and structurally heterogeneous across sectors?

Each of those adjectives is doing real work, and each corresponds to a feature that simpler approaches handle poorly or not at all:

Nonlinear drift. A plain OU process pulls back with a force proportional to the deviation. The package allows a cubic correction, so the restoring force can strengthen super-linearly when prices are far from equilibrium. This matters: real markets may behave gently near the center and violently at the extremes, and a linear model cannot represent that.

Stochastic volatility. Financial data, and economic data generally, go through quiet stretches and turbulent ones. The package does not assume a single noise level; it lets the volatility itself wander over time, following its own mean-reverting process on the log-variance. This is the same idea that powers modern stochastic-volatility models in finance, and it is essential for not fooling yourself about the precision of your estimates.

Heavy tails. Economic shocks are not Gaussian. Crashes, booms, and policy shocks produce outliers that a normal distribution would call essentially impossible. The package uses Student-t innovations and estimates the degrees of freedom from the data, so the model can discover for itself just how fat-tailed the world is.

Hierarchical structure across sectors. An economy has dozens of sectors, and each one presumably has its own reversion speed, its own equilibrium, its own noise. Estimating each sector in isolation throws away the information that they are all part of the same economy. Estimating them all with one set of parameters pretends they are identical. The package takes the middle path — hierarchical, or “partial pooling,” priors — where each sector’s parameters are drawn from a shared distribution whose properties the model also estimates. Sectors borrow strength from one another without being forced into lockstep.

A time-varying coupling. This is the most economically loaded feature. The strength with which market prices track prices of production is allowed to depend on the aggregate profit rate (what the package calls TMG). When the general rate of profit is high, the pull of production prices on market prices may be one thing; when it is low, another. Whether that modulation exists, and in which direction, is a hypothesis the model can test rather than assume.

All of this is estimated jointly, with full Bayesian uncertainty, using Stan’s Hamiltonian Monte Carlo sampler. You do not get a point estimate of the reversion speed; you get a posterior distribution, and from it a credible interval and a probability statement like “there is a 95% chance the half-life is between six and eighteen years.”

The nested cascade

The second model is the more ambitious one, and it is where the package earns its “nested” branding. Instead of market prices reverting to a fixed equilibrium, they revert to a latent production price — a hidden, unobserved series that itself evolves over time according to its own OU process, driven by the general profit rate. And, if you turn on the third level, that latent production price in turn gravitates around an observed “value” index built directly from labour-content accounting.

So the full structure is a cascade: market price → latent production price → value. Each arrow is an OU reversion, each with its own speed, and the speeds are constrained so that the outer (market) layer reverts faster than the inner (production) layer — an economically natural separation of timescales, enforced softly so the data can push back.

The reason this matters is that it converts a slogan — “prices of production gravitate around values” — into a literal statistical hierarchy that can be fit to data and compared against alternatives. The headline empirical result, from a fit to 37 US sectors over 1960–2020, is a value-coupling coefficient essentially equal to one, with the posterior probability of it being positive effectively equal to one. In plain terms: in standardized units, prices of production track labour values almost one-for-one. That is a found result, not an assumed one — the prior on the coupling was centred at zero, deliberately neutral.

The inference engine, and why it is not a footnote

It would be easy to glance at the model description, nod, and move on. But how these quantities are estimated is half of what makes the package serious, and it is worth a paragraph for readers who do not think about MCMC every day.

Bayesian inference works by exploring the space of all parameter values consistent with both the data and the prior, and characterizing that space as a probability distribution. For models this complex — with latent volatility paths, hierarchical structure, and hundreds of parameters — you cannot do that with pencil and paper. You use a Markov chain Monte Carlo sampler, specifically Hamiltonian Monte Carlo, which borrows an idea from physics: give the parameter space a “potential energy” (the log-posterior) and a “kinetic energy” (a randomly chosen momentum), and let the system glide around the posterior like a ball rolling over a landscape.

Stan’s NUTS sampler automates this about as well as it can be automated, and the package uses it with within-chain parallelism (via Stan’s reduce_sum) to handle the fact that the likelihood must be summed over many timepoints and sectors. The diagnostics — R-hat for chain agreement, effective sample size, divergence counts — are surfaced through a validate_ou_fit function, and the package is explicit that you should look at them before believing anything.

Model comparison is done with PSIS-LOO, a clever technique that approximates leave-one-out cross-validation without refitting the model dozens of times, by reweighting the posterior draws using importance sampling. It is the modern standard, and the package is appropriately cautious about it: because the model has a latent volatility state at every observation, plain LOO is known to be optimistic, and the documentation says so plainly.

The honesty that makes it credible

Here is where the package surprised me, and here is why I think it deserves a wider audience than the Marxian-economics niche it lives in.