Political Economy • Econometrics • Marx

Was Marx Wrong About Prices of Production?

A 260-Page Investigation Says No.

How one researcher spent years showing that the most famous critique of Marx’s economics rests on a mistake Marx never made.

A Fatal Flaw, or a Fatal Misreading?

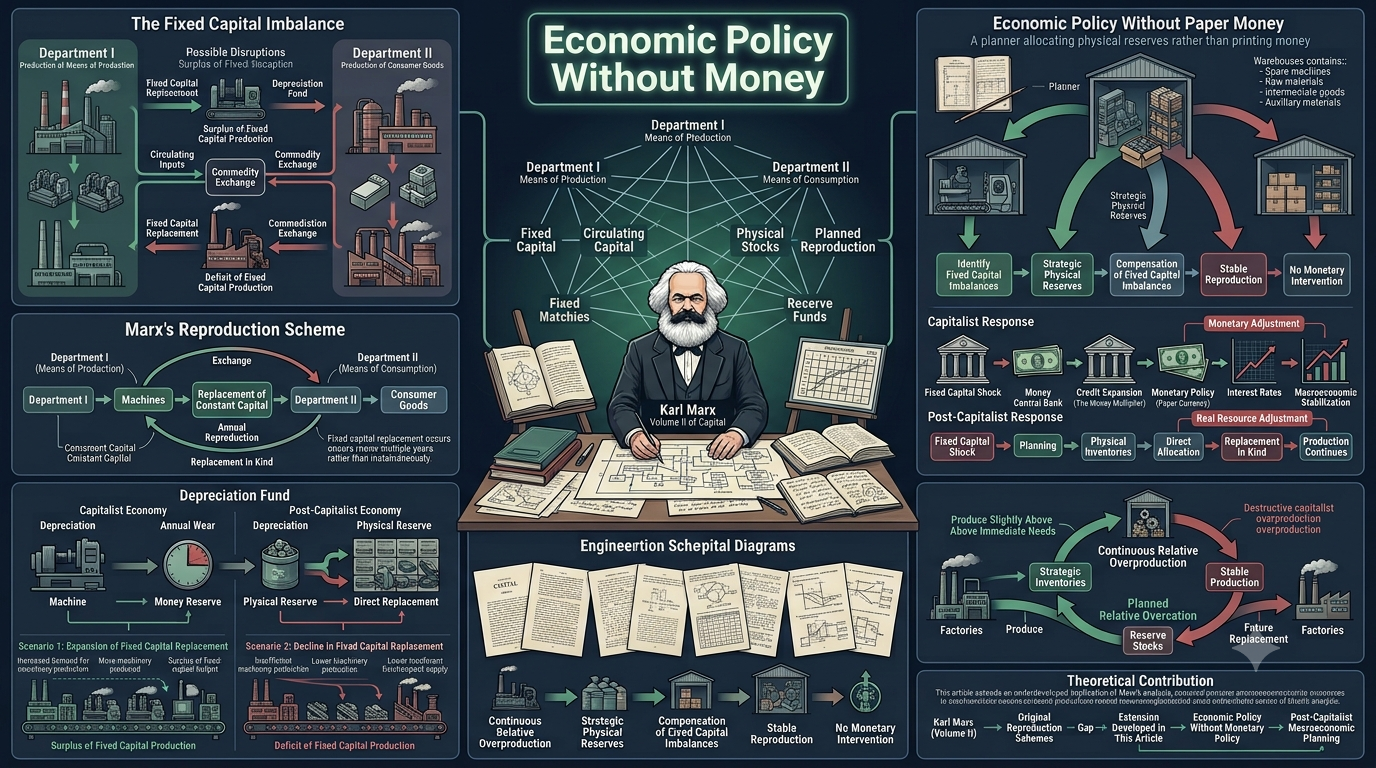

For over a century, a single mathematical argument has been wielded as the definitive proof that Karl Marx’s economics doesn’t work. It goes like this: Marx claimed that the value of goods is determined by the labor that produces them, and that market prices eventually gravitate toward “prices of production” — modified versions of those labor values, adjusted for how capital-intensive each industry is. But when you try to verify this with a system of simultaneous equations, the numbers don’t add up. The sums of values don’t equal the sums of prices. The theory, critics have said since the early 1900s, contains a fatal algebraic error.

This paper — spanning 260 pages and drawing on philosophy, history, sociology, and statistics — argues that the error was never Marx’s. It was the error of the people who checked his math using a method he never used.

The Photograph vs. the Movie

Imagine you’re trying to understand a river. You could take a photograph of it — capturing one frozen moment — or you could film it as a movie, watching how the water flows over time. For over a hundred years, the economists who criticized Marx took a photograph of his theory and then complained that it didn’t look like a movie.

Here’s the specific issue. Marx described a two-step process: first, a general rate of profit forms across the entire economy; then, each industry’s price deviates from its pure labor value according to how much capital it ties up relative to the average. The standard critique — originating with Ladislaus von Bortkiewicz in 1907 and repeated ever since — takes all of Marx’s accounting identities and solves them simultaneously, as if input prices and output prices were determined at the same instant. Under that framework, Marx’s three aggregate equalities cannot all hold at once.

But here’s the catch: solving everything simultaneously is equivalent to assuming that the economy is a photograph — that there is no time. And Marx’s entire framework is built on the opposite premise: that the economy is a process, an unfolding sequence in which the prices that exit one period become the input prices that enter the next. Once you restore that temporal dimension, the “inconsistency” vanishes. The three equalities hold simultaneously — not because Marx was secretly consistent in some miraculous way, but because the contradiction was an artifact of the framework imposed on him, not of his own logic.

The paper calls the simultaneous approach “Walrasian Marxism” — a phrase that captures the irony: economists imported the logic of Léon Walras’s general equilibrium theory and used it to read Marx, then blamed Marx when the result didn’t work.

Marx was accused for over a century of getting the arithmetic wrong. What actually happened is that someone redid his arithmetic under an assumption he never made — that the prices of things you buy to produce and the prices of things that come out of production are the same prices, set at the same time. If you assume that, Marx’s accounts don’t close. But that assumption is equivalent to saying the economy doesn’t happen in time.

But Was the Movie Real?

Pointing out that Marx’s logic works when you read it correctly is necessary but not sufficient. The “temporalist” school has been making this argument for nearly fifty years. But the author noticed a critical gap: nobody in that school had ever taken real-world data and actually estimated the three types of prices Marx described — direct labor values, prices of production, and market prices — and then tested whether market prices actually gravitate toward prices of production as the theory predicts.

This matters because, as the paper puts it, leaving the correct reading of Marx “in the territory of conceptual argumentation while the incorrect reading occupies alone the territory of measurement” is a strategic vulnerability. If you can’t show that real prices behave the way your theory says they should, your theory remains a philosophical argument, however internally consistent.

But before presenting any numbers, the paper devotes substantial space to establishing that the process Marx described actually happened in history. This is not an appendix; it’s a foundational part of the argument.

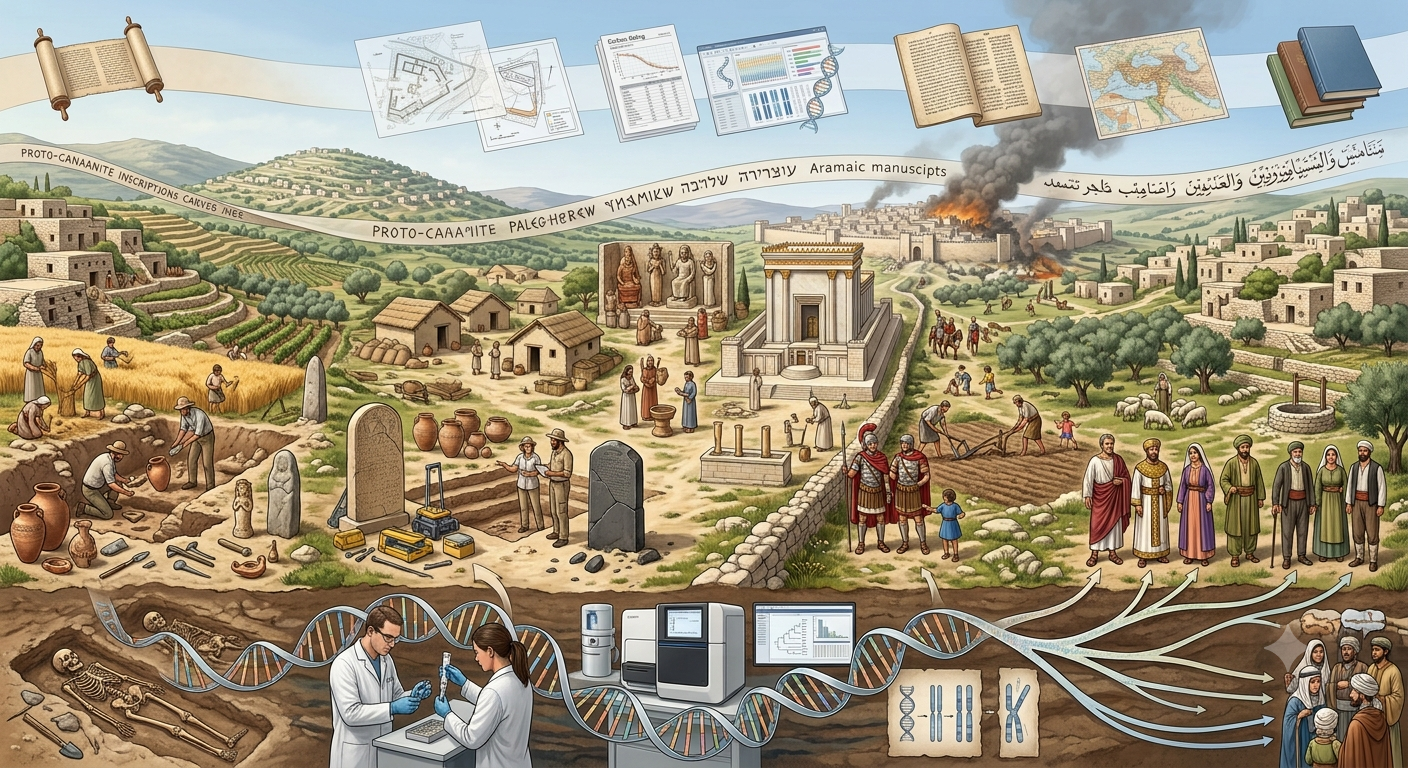

Before Capitalism

In pre-capitalist societies, exchange was regulated by labor time — not because someone enforced a theory, but because the material conditions made it so. Barter was dominant, inflation did not exist, and prices could only reflect production costs given available technology. Evidence from anthropology (Malinowski’s Trobriand Islands studies), sociology (Mauss on gift exchange), accounting history (Kula’s analysis of feudal estate records), and even paleogenomics all converge: objects were valued in proportion to the labor they embodied.

The Transition

The dissolution of feudal relations, the monetization of exchange, and the destruction of pre-industrial normative frameworks created the conditions for capital to move freely between industries. Thompson’s work on the “moral economy” documents how the new free-market ideology had to be violently imposed, destroying customary protections and creating an unprecedented relationship of exploitation.

Capitalism Established

Once barriers to capital movement were destroyed, capital flowed from commerce to industry chasing higher profits, and generalized competition forced a redistribution of total surplus value across sectors. The crisis of 1873 — which destroyed nearly half the blast furnaces in major iron-producing countries — is presented as concrete evidence of the mechanism: firms whose costs were still based on older, individually more labor-intensive methods went bankrupt when they couldn’t compete with prices of production dictated by modern technology.

Prices of production didn’t appear the day someone wrote an equation. They appeared the day capital could freely move from one industry to another chasing the highest profit — which didn’t happen until legal, moral, and political barriers were destroyed. Before that, things were exchanged roughly according to the labor they cost, and there is more than enough evidence — ethnographic, accounting, archaeological, and genetic — to show it.

What Is a Production Price, Exactly?

This is where the paper moves into its most technically original territory. The author carefully separates two things that must not be confused:

What a production price is (the explanandum): it is the expected value, over the distribution of economic perturbations, of the long-run time average of market prices. In plain language: it’s the center of gravity around which actual market prices keep spinning. Not the price they arrive at and stay at (that would be equilibrium), but the average around which they never stop oscillating.

The production price is neither an eternal, timeless equilibrium (the error of the simultaneous approach and of Walrasian economics, which takes the law as such for the whole and eliminates time) nor a chaos of prices without law (the error of empiricism, which stays at the level of individual prices and loses the law). It is the law of the whole realizing itself through the contingency of the parts.

How each step of the process works (the explanans): a rule that determines this year’s market price from last year’s market price and last year’s latent production price, and nothing else. This is modeled as a hierarchical Ornstein-Uhlenbeck process — a three-level cascade in which the production price is itself a latent state with its own dynamic gravitating toward value, and market prices gravitate toward that latent state rather than toward a fixed, noisy index.

The uncertainty is built into the model explicitly: uncertainty in the average rate of profit, uncertainty in the advanced capital, uncertainty in the disaggregation of national accounts into 37 sectors (handled through multiple imputation with 25 imputations combined by Rubin’s rule), and parametric uncertainty estimated through Bayesian Markov Chain Monte Carlo methods.

One crucial point: no magnitude is obtained by solving a simultaneous system. Value is constructed empirically and directly as $V = c + v + p$ (cost plus surplus value), and production price as $\Phi = c + K \cdot G’$ (cost plus capital times the general rate of profit). There is no Leontief inversion, no simultaneous algebra, anywhere in the construction.

Think of a production price as the “gravitational center” of a spinning object. The object (a market price) never stops moving — it wobbles, it swings, it drifts — but over time its average position is pulled toward that center. The math describes both what the center is and how each wobble happens, and it does so while honestly accounting for all the uncertainty in the measurement.

The Defining Equations: (9) Through (11)

Here is where the metaphor turns into mathematics. The paper writes the definition of a production price in three successive steps — each one making explicit an assumption the previous step left implicit — numbered (9), (10), and (11) in the original text. None of the three generates a trajectory by itself; together they define the explanandum — what the object is — that the cascade below then generates.

Here $\varphi^i_t$ is sector i’s market price at time $t$, $k^i_t$ is its cost price (constant capital consumed plus variable capital), $K^i_t$ is the total capital advanced, and $G'(t,X)$ is the general rate of profit — itself a stochastic process indexed by a perturbation $X$ that bundles the exodus of capital between branches and technological innovation.

In words: a production price is the long-run limit of the average market price. Not the price itself at any instant — that keeps oscillating forever — but where its time-average settles as the horizon stretches out. Notice the object on the right-hand side, $k + K \cdot E[G’]$: it is the same accounting identity introduced earlier (cost price plus the average profit rate applied to capital advanced), except the profit rate is now written as an expectation, because it fluctuates.

$f_X$ is the probability density of $X$. The equation says the expectation is an average over every possible state $x$ of the system’s turbulence, weighted by how likely that state is.

Equation (10) earns its keep by making a subtle move legitimate: swapping the order of the limit and the expectation. That looks harmless, but it hides a real question — does the market price $\varphi^i_t$ even converge to anything as $t \to \infty$? The paper’s answer is no: a capitalist system doesn’t settle into a fixed point, it settles into a limit cycle — perpetual oscillation. So the convergence the argument needs isn’t of the instantaneous price, but of its cumulative time-average. That average does converge, for almost every state of the world, precisely because the system is ergodic — the fraction of time the cycle spends in each region of its orbit stabilizes. This is the Birkhoff ergodic theorem doing, in mathematical language, exactly what Marx says in economic language: the production price isn’t the value the market price reaches and stays at, it is the average around which it never stops oscillating. The oscillation isn’t an obstacle to the average — it is the average’s condition of existence.

The paper invokes Lebesgue’s Dominated Convergence Theorem to justify swapping “limit of the average” for “average of the limit.” This requires bounding market prices by some integrable envelope — economically, that no price can grow without limit, which technological ceilings and competitive pressure guarantee — and, crucially, it does not require that the convergence be uniform across sectors. Uniform convergence would mean competition equalizes profits instantly and identically everywhere, with no room for a shock to hit one industry harder than another. Marx’s theory says the opposite, and the math is built to allow it.

Equation (10) still treated the capital base $K^i_t$ as known exactly. Equation (11) drops that simplification: $Y$ is a second random variable carrying the estimation error in $K$, with density $f_Y$, and $f_{X \mid Y}$ lets the profit-rate perturbation depend on which realization of that error occurred. The object is the same double average — only now uncertainty is propagated from two sources instead of one.

This last equation is not a mathematical flourish; it is the reason the empirical section spends so much effort on multiple imputation. National accounts don’t hand anyone a clean measurement of capital advanced by sector — it has to be reconstructed from incomplete data, and that reconstruction carries its own error. Equation (11) is the license to treat that error as a random variable to be averaged over rather than a nuisance to be ignored. The uncertainty is propagated externally — by a generator outside the statistical model itself — rather than estimated as an internal parameter of the dynamic model: estimating $K$’s error inside the model would confound it with the model’s own measurement-noise term, opening a ridge of non-identification between two magnitudes that the data alone cannot tell apart. Kept external, twenty-five complete reconstructions of the data are generated first, each respecting the Marxian aggregate identities to machine precision, the dynamic model is fit on each, and the twenty-five fits are combined by Rubin’s rule. That is the outer average of equation (11), computed by literally drawing from the distribution of $Y$ instead of assuming it away.

The Engine: A Three-Level Ornstein–Uhlenbeck Cascade

Equations (9)–(11) define the target; they don’t generate a path toward it. The explanans — the mechanism that actually produces a year-by-year trajectory consistent with that target — is a hierarchical Ornstein-Uhlenbeck process with up to three nested levels, fit as a single Stan program (the same program handles one, two, or three levels, which guarantees that adding levels can never silently break the simpler cases nested inside them). All series enter standardized; time is discretized one year at a time using the Euler–Maruyama scheme.

Subscripts $s$ (sector) and $t$ (year) run throughout. $dev$ is last year’s gap between market price and the latent production price. $\kappa^m$ is the sector’s reversion speed, passed through a logit link that caps it inside $(0, \kappa_{\mathrm{cap}})$ and lets the general rate of profit ($z^{TMG}$) modulate it without ever pushing the system out of the stable region of the discretization. $\varepsilon$ is a fat-tailed (Student-t), stochastic-volatility innovation, so volatility can cluster in time without destabilizing the mean.

Read the Level 1 line as a spring. The term $-\kappa \cdot dev$ is the restoring force: it pulls the market price back toward the production price with a force proportional to how far it has drifted. The cubic term $a_{3,s} \cdot dev^3$, with $a_{3,s}$ constrained negative by construction — not estimated, imposed — makes that restoring force grow faster than proportionally once the deviation gets large: the further the market strays, the harder it snaps back. This is a declared stability assumption, not a discovery: it guarantees the model can never generate an explosive regime, at the real cost that if such a regime existed in some sector of the actual economy, this particular specification could not detect it.

The production price $\Phi$ is not treated as a fixed, observed index; it is itself a latent state that reverts — more slowly, with its own sector speed $\kappa_p$ — toward this mean $\mu$. $m_1$ is the channel running through the general rate of profit; $m_v$ is the coefficient measuring how strongly the production price tracks the directly-constructed value $V_{s,t} = k + p$ (Level 3, and the reason the cascade goes up to three levels rather than stopping at two).

This is the bridge back to the abstract equations above, term by term. $\mu_{s,t}$ is the estimable stand-in for the right-hand side of (9): $m_{0,s} + m_1 G’_t$ plays the role of $k + K \cdot E[G’]$, and $m_v V_{s,t}$ is the specific functional form chosen for the value-tracking channel that the abstract definition deliberately leaves open (the paper is careful to say that capitalist competition as a function of the value structure is declared at the level of equations 9–11, not derived; giving it the concrete shape $m_v V$ is a modeling choice made at the cascade level, defended by how it performs under validation rather than deduced from the definition). And the expectation of $G’$ from equation (9) has its operational counterpart in the profit rate averaged across the twenty-five multiple imputations — the mechanism equation (11) licenses.

The coefficient $m_v$ carries real theoretical weight: it is the empirical stand-in for Chapter 9’s claim that prices of production gravitate around values. It is given a neutral prior, $m_v \sim \mathcal{N}(0,\, 0.5)$ — centered at zero, symmetric, assigning equal plausibility to $m_v > 0$ and $m_v < 0$ before seeing any data. That matters for the same reason a fair coin matters in a coin-flip experiment: if the data carried no signal, the posterior would sit wherever the prior put it, hugging zero. It doesn’t. It lands at $m_v \approx 1.0136$ with $P(m_v > 0) = 1$ — evidence that the data moved it there, not the prior. The anchoring to value is found, not assumed into the setup.

The cascade is three springs stacked on top of each other. The market price is tied by a spring to the latent, unobserved production price. The production price is tied by its own, slower spring to a moving target that blends the general rate of profit with the directly-measured labor value. Pull any one spring and let go: it doesn’t snap to a fixed point, it settles into the kind of perpetual, decaying oscillation that equations (9)–(11) describe as an average. The springs are estimated from sixty-one years of real U.S. data, not assumed; the coefficient tying prices of production to values, specifically, could have come back negative or zero — the model gave it every chance to — and it didn’t.

What the Numbers Say

The empirical core of the paper is a panel of 37 productive branches of the United States economy over 61 years, from 1960 to 2020. The hypothesis tested encloses three distinct relationships, and the paper is meticulous about not conflating them. Each is stated, tested, and reported separately.

Market Prices ↔ Prices of Production: The Strongest Link

This is the relationship with the firmest statistical support, confirmed through six independent lines of evidence:

Gravitation exists, and it is slow. The median speed across sectors is $\kappa_m = 0.0770$, equivalent to a half-life of approximately 9 years. Market prices take about a decade to cover half the distance toward their production-price center. This is consistent with Marx’s characterization of gravitation as a tendential, mediated regulation, not an instantaneous fit.

The number is remarkably stable under stress tests:

- Removing five of the six productive blocks from the panel barely moves the estimate — it shifts in the third decimal place. The sixth, which gathers 18 of the 37 sectors, does produce a shift (from 9 years to 6 years), and the paper decomposes it: about half the acceleration is the generic effect of halving the panel — removing 18 sectors at random already gives 0.0929 — and not the block itself.

- Dismantling the value anchor in three different ways — including permuting surplus value across spheres — moves the speed in the third decimal place. This is significant: it means the conclusion about market-to-production gravitation does not depend on the less robust production-to-value link.

- The market deviation has its own dynamic signature. Compared against a random walk matched in variance, three out of six test statistics separate cleanly (the weighted-sum convergence reaches a tolerance of 0.01 while the null never reaches a tolerance ten times more lenient; recurrence analysis laminarity triples the null; recurrence entropy doubles it). The ones that don’t separate are recurrence-analysis determinism and the two deterministic-chaos invariants — the Lyapunov exponent and the correlation dimension — which the paper never claimed to find.

- The estimate is invariant to secondary methodological choices. Sweeping the latency regularizer across three values produces life medias of 9 years in all three arms (speeds of 0.0774, 0.0770, 0.0772).

- The known bias of disaggregation pushes against the result. Splitting a national figure among 37 branches is underdetermined and biases speed estimates downward — meaning the true half-life is probably 7–8 years rather than 9. A bias that works against your conclusion is one you can live with, because the result holds despite it, not thanks to it.

Prices of Production ↔ Values: The Thinnest Leg

This is the weakest part of the empirical argument, and the paper states so with complete transparency. The problem is not a defect of the instrument but a property of the object:

The coupling coefficient estimated within the dynamic model is $m_v = 1.0136$ with a 95% credible interval of $[1.0096,\; 1.0176]$ — but the same procedure returns 1.0365 when surplus value is permuted across spheres, preserving all annual aggregates. Why? Because production price and value share the cost price, which explains 66.1% of the variance of the former and 72.0% of the latter, and their correlation in levels is 0.9987. The coefficient would land near one even if the law of value didn’t hold at all. The paper therefore reports it as a consistency check, not as evidence.

The real support for this relationship comes from cross-sectional tests, not from the dynamic coupling. When temporal common trends are removed and analysis is conducted within-year, the slope of the markup on own surplus value is 0.675 with the true data versus 0.090 under permutation, with intervals that don’t come close to overlapping. The sectoral ordering of the wedge between $\Phi$ and $V$ has an inter-annual rank correlation of 0.986 and a 60-year value of 0.558 — highly persistent structure, not noise.

A collateral finding worth noting: the coefficient of variation of sectoral profit rates is 0.669 — meaning profit rates across industries show considerable and persistent dispersion. Far from contradicting the theory, this dispersion is the condition of existence of the mechanism: if profit rates were already equalized, there would be no differential to drive capital migration, and gravitation would have nothing to operate on. Marx postulates equalization as a tendency, not an accomplished fact.

Market Prices ↔ Values: Sustained in Form, Adjusted in Existence

The structural modification across sectors exists and is nonlinear (the nonlinearity step holds comfortably at 6.8 null deviations). But the existence step is adjusted: 44% of its gain is obtained equally with sectoral characteristics unpaired from their spheres, and the gap against the maximum null is on the order of one paired standard error. The coefficients survive a deliberately severe correction for serial dependence (tripling the error).

That test is a small ladder of nested distributional-regression models, fit with gdpar (Gómez Julián, 2026b), the author’s own R package for generalized distributional parameter regression, published on CRAN on July 15, 2026. The ladder climbs from a bare model — “the market-to-value ratio has no sector-specific correction at all” — through a model where organic composition, wage share, and sector size shift that ratio linearly, up to a model where the correction is a flexible spline rather than a straight line. Two gains matter, measured in units of predictive density: adding the linear correction buys 207.3 units; letting it curve buys another 215.1. Both were checked against a control built to be hard to pass — shuffling which sector gets which characteristics 99 times, refitting each time, with the spline’s knots held fixed across every shuffle so the comparison can’t be won by a better basis alone. The curvature gain clears its null with room to spare (6.8 null standard deviations; the best of 99 shuffles reaches only 114.8 against 215.1 observed). The existence gain is honestly reported as thinner: shuffled sectors still buy about 44% of the real gain merely by having some characteristics to fit — three covariates and an intercept give a model room to accommodate noise even when it is being told nothing true — so the genuine margin over the null sits at about one paired standard error (23.2, against a gap of roughly 24 units). Both numbers are reported together, precisely so the large one isn’t read alone.

A companion specification, estimated in the same gdpar fit, asks the same question about dispersion rather than location: not where the market-to-value ratio is centered, but how tightly it clusters. Larger sectors and sectors with higher capital composition show systematically less relative dispersion — elasticities of $-0.226$ and $-0.104$ — consistent with equalization operating more effectively where capital is more concentrated. Both effects clear a “breaking factor” (the multiple of the standard error at which the 95% interval would first touch zero) north of six and four respectively, past the 2.94 ceiling reached anywhere else among this paper’s location coefficients, and the finding reproduces under a completely different likelihood family (a gamma distribution on the price ratio) to within 5.2%.

Three Failures That Confirm the Theory

One of the most intellectually striking features of this paper is how it handles results that, at first glance, look bad for its thesis. There are three, and the paper reports all of them without softening — then shows deductively why each one was expected if the theory is correct.

The model does not out-of-sample predict better than a random walk. But this was deductively implied by the slow form of the thesis. At a horizon much shorter than the half-life, a mean-reverting process is, to first order, a random walk. If something takes a decade to get halfway back, looking at a single year won’t let you see it return.

The value term is predictively indistinguishable. Again, this follows from the slow coupling between prices of production and values: with half-lives on the order of decades and only 61 years of data, univariate root-unit tests are structurally underpowered.

No univariate test separates the true wedge from its permuted placebos. But this was predicted before measuring, by the persistence of sectoral ordering itself (inter-annual rank correlation of 0.986). A highly persistent time series is hard to distinguish from its permuted version using tests designed for shorter memory.

The paper’s stance on this is worth highlighting: “Lejos de refutar la tesis, los tres están deductivamente implicados por su forma lenta” — far from refuting the thesis, all three are deductively implied by its slow form. A single mechanism (slow gravitation) explains both the substantive thesis and all the apparently negative results, and it also survives in the validated posterior. “That a single cause explains the thesis and all the apparently negative results, and that it additionally survives in the validated register, is the opposite of a petitio principii: it is a unified, falsifiable, and internally validated narrative.”

Temporalism Isn’t a Preference — It’s a Condition of Measurement

Perhaps the most consequential result in the entire paper is not a number but a statement about what can and cannot be measured. It concerns the “modulator” — the component of Marx’s argument in which the general rate of profit enters into the structural modification of each sphere, meaning the deviation of each sphere is not independent of the reference but generated by it.

When the model was run with a single, fixed general rate of profit for all 61 years (as a simultaneous approach would require), the posterior exhibited a flat ridge: two completely different functional bases (a degree-two polynomial and a spline basis) produced the same pathology to the third decimal place, with an effective sample size of only six draws. The diagnostic got worse with more sampling (R-hat rising from 1.33 to 1.73). This is the unmistakable signature of a direction in parameter space along which the likelihood does not change.

The cause is theoretical, not computational. With one fixed reference, the modulator can only be identified evaluated at that single point — a single number, not a function over the space of references. You cannot estimate three coefficients from a polynomial if you have one data point.

When the reference was allowed to vary year by year (61 different general rates of profit), the model converged within minutes, with a large improvement in both time and effective sample size, and zero divergences.

This diagnosis isn’t an ad hoc read of a misbehaving sampler. gdpar (Gómez Julián, 2026b) — the same package behind the nested ladder above — ships a formal identifiability result for exactly this situation. Its Theorem 1A establishes that, with a single fixed reference point, a distributional modulator is identified only at that point: as one number, not as a function over the space of possible references. Theorem 1E is the positive counterpart: letting the reference vary restores identifiability of the modulator as a function. Fitting a degree-two polynomial (three coefficients) or a five-knot spline basis (five coefficients) against one single, unmoving reference asks for more than a single data point in that dimension can support — which is exactly what a flat likelihood ridge looks like from the sampler’s side.

The figures behind the improvement, precisely: a fixed reference with a degree-two polynomial gives an R-hat of 1.7333, an effective sample size of 6, and 8 divergent transitions in 39 minutes; a one-knot spline basis reproduces the same pathology — R-hat 1.7335, effective sample size 6, 14 divergences, 5.6 hours. Letting the reference vary year by year (61 distinct annual values of the general rate of profit), centering the additive component and raising the sampler’s adaptation parameter to 0.99, gives an R-hat of 1.0035, an effective sample size of 1332, and zero divergent transitions — in 2.9 minutes. That is the 115-fold improvement in time and 222-fold improvement in effective sample size referenced above, and it is a theorem, not a tuning trick: no amount of additional sampling closes that gap under a fixed reference, because the object being asked for — the modulator as a function — simply is not there to find.

The consequence is stated precisely: with a single fixed general rate of profit obtained by solving the system simultaneously, the claim of Chapter 9 of Volume Three of Capital is unverifiable by construction. It is not that the data are insufficient — the object is not identified, and no amount of data would identify it. The argument does not establish that simultaneism is false as a description of capitalism (that is established by historiography and sociology); it establishes that a simultaneous procedure cannot, even in principle, empirically verify the specific part of Marx’s argument that this work estimates.

Marx says: first a general rate of profit forms, then each industry deviates from it according to how capital-intensive it is. To check whether the deviation depends on the general rate, you need to see what happens to the deviation when the general rate changes. If you calculate one general rate for the entire 61-year span, it never changes, and there is nothing to observe. That is exactly what happened: the model with one fixed rate doesn’t converge — not because of computational limitations, but because it is being asked to measure a relationship with a single observation of one of the two variables. Calculating one rate per year — which is what the temporal reading says you should do — the same model converges in three minutes.

What This Is, and What It Isn’t

The paper is careful, almost painstakingly so, about the limits of what it claims. This section matters because a reader coming from the “pro-Marx” or “anti-Marx” side might be tempted to over-read the results. The author doesn’t let you.

What the evidence authorizes: In the United States between 1960 and 2020, market prices gravitate toward prices of production with a decadal half-life that is sectorially heterogeneous, and this speed survives three independent assaults (removing five of the six productive blocks, destroying the value anchor, varying secondary methodological decisions). This is a measured, calibrated, and falsifiable fact.

What the evidence does not authorize:

- It does not claim superior predictive power (the model does not out-predict a random walk, which was expected).

- It does not claim that univariate root-unit tests confirm gravitation (they are structurally underpowered at this time scale).

- It does not claim uniqueness or categorical novelty. The contribution is the explicit integration and canonization of a slow gravitation cascade with value anchoring, measured on real data, with propagated uncertainty, validated, and subjected to a diagnostic whose unfavorable results are reported alongside the favorable ones.

- It does not claim that this statistically demonstrates the law of value, “and not for rhetorical prudence but because it would be false: a price series can show that a magnitude behaves as the law predicts, and cannot explain why that magnitude exists or whether the category with which we name it is the correct one.”

That last point is the paper’s deepest epistemological commitment. Questions about whether “value” is the right category for what prices ultimately measure are not answerable by any price series, no matter how long. They are answered by history, sociology, and philosophy — and the firm answer is the one obtained when all four disciplines (those three plus statistics) point in the same direction. The four-dimensional convergence is the argument, not any single leg of it.

The paper also addresses the homology that unifies its seemingly disparate halves — the historiographical-filosofical first chapter and the econometric second chapter. The relationship between necessity and contingency that governs the transition from feudalism to capitalism (where the same demographic shock produced opposite outcomes in different regions of Europe) is structurally identical to the relationship between prices of production and market prices. A law determines the center; circumstances determine each particular outcome. Neither fact negates the other, because they describe different levels of the same reality.

What It All Adds Up To

Here is the simplest version of what this 260-page paper establishes:

But recognizing the conceptual error was only the first half. What had been missing — and what this paper contributes — is doing those accounts with real data instead of with fictitious numerical examples, which is what the school that had the correct conceptual reading had never done.

The empirical results show that prices in the U.S. economy over six decades do behave as the theory predicts: they gravitate, slowly, toward prices of production calculated with Marx’s theory and no other. This finding survived every attack the author could devise — removing productive sectors, destroying the value anchor, permuting surplus values, varying methodological decisions, and running diagnostics whose unfavorable results are reported in full alongside the favorable ones.

The part of the argument linking prices of production to labor values is also supported by real evidence, though less firmly, and the paper says exactly where the weak points are and why they are properties of the object, not defects of the instrument.

And the paper does not claim to have demonstrated the law of value with a series of numbers, because “questions of that kind are not answered with numbers: they are answered with history, with sociology, and with philosophy, and the firm answer is the one obtained when the four things (the previous three, together with statistics) all point in the same place.”

That convergence doesn’t make the result eternal — better evidence can overturn it tomorrow. But it makes it, for now, “our best possible approximation to the truth.”

“In science as in life, overcoming adversity is what makes us truly strong.”

This post summarizes the introduction, conclusions, and the formal-empirical chapter (§2.4) of Gómez Julián, J. M. (2026). Some Reflections on Marx’s Prices of Production: Historicity of the Law of Value, Dialectical-Materialist Foundation, and Dynamic Formalization Under Uncertainty. Zenodo. https://doi.org/10.5281/zenodo.21842251. The full paper spans approximately 260 pages across two chapters covering philosophy, historiography, mathematical formalization, and empirical econometrics. Equations (9)–(11) and the model specification cited here reproduce that chapter’s notation; gdpar is cited separately as Gómez Julián (2026b).

Written for the curious. An invitation to read.