Marxist Economics · Econometrics · Political Economy

What Counts as “The Economy”?

A Marxist Framework for Measuring Capitalism’s Rate of Profit

How one researcher built a theoretically rigorous rulebook for a question everyone answers differently — and what happens when you let the data decide for itself.

Based on: Gómez Julián (2025)

|

~12 min read

|

Originally published as a preprint on arXiv

In 1984, two economists named Anwar Shaikh and Edgardo Ochoa opened a research tradition that would span four decades: empirically measuring Marx’s most consequential prediction — that capitalism’s average rate of profit tends to fall over time. Since then, dozens of studies have followed, each arriving at the same fundamental calculation, but each choosing differently which sectors of the economy to include. Some count everything. Others exclude finance and government. Still others carve out a narrower productive core. The results? They disagree — sometimes dramatically — about whether the profit rate actually falls.

The problem isn’t sloppy math. It’s that nobody has ever agreed on a standard for deciding which economic activities belong in the calculation. José Mauricio Gómez Julián’s recent paper aims to change that.

◆

The Question Nobody Agrees On

Here’s the issue in plain terms. Suppose you want to calculate the “average rate of profit” for the entire U.S. economy over sixty years. You need two things: the total surplus value produced and the total capital invested. To get these, you aggregate data from individual sectors — agriculture, manufacturing, finance, retail, government, and so on.

But should finance be in there? Finance doesn’t manufacture anything; it redistributes money. Should government? The government doesn’t compete for profits. Should retail trade? A retailer buys finished goods and sells them at a markup, but Marx argued that the act of buying and selling doesn’t create new value — it merely realizes value already embedded in the commodity.

These aren’t arbitrary questions. If you include sectors that redistribute value rather than create it, you can artificially inflate or deflate the measured profit rate, potentially masking the very tendency Marx predicted. Different researchers have made different choices, and the field has lacked a unified standard — until this paper.

◆

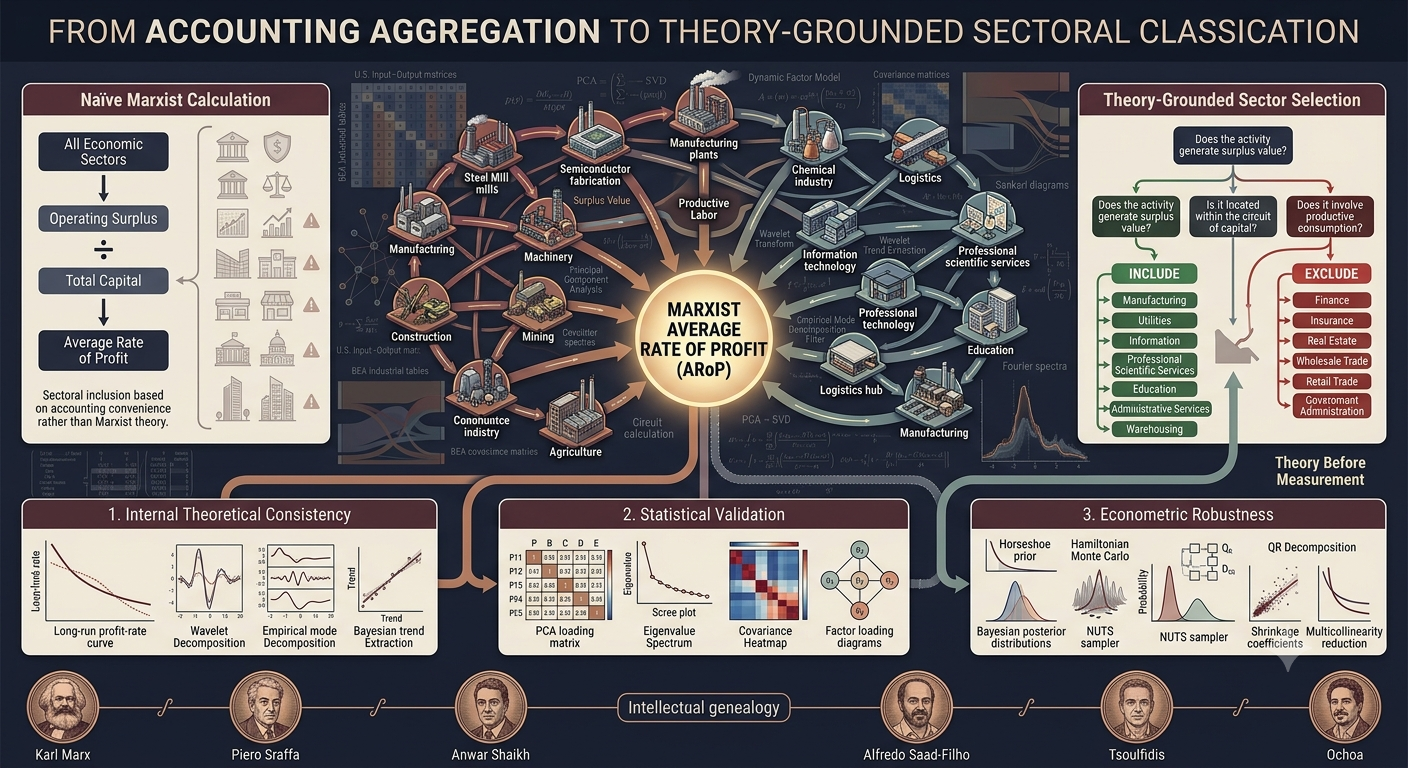

Three Pillars: The Theoretical Logic Behind the Criteria

Gómez Julián’s framework is built on three interlocking concepts from Marx’s political economy. The underlying logic of the entire procedure can be stated simply: an economic sector should be included in the average-rate-of-profit calculation if, and only if, its workforce performs productive labor as Marx defined it — labor that is subordinated to capital and directly produces surplus value, or that constitutes an indispensable material condition for that production to occur. Everything else is excluded.

Let’s walk through each pillar to see how this logic unfolds in practice.

1. Productive vs. Unproductive Labor

The most fundamental distinction in Marx’s economics is between labor that creates value and labor that doesn’t. Productive labor, in the Marxist sense, isn’t about whether work is “useful” in everyday language. It’s a technical category: productive labor is work performed under the subordination of capital that produces surplus value — the unpaid portion of the working day that capitalists appropriate for free.

Unproductive labor, on the other hand, doesn’t generate new value. It may be socially necessary (think of a cashier or an accountant processing invoices), but it merely facilitates the transfer or realization of value that was already created elsewhere in the production process. It is, as Marx called it, a faux frais — a cost that must be paid out of surplus value rather than one that generates it.

The mere functions performed by capital in the sphere of circulation — the operations necessary to serve as the vehicle for the metamorphoses of commodity-capital — do not create value or surplus value.

— Karl Marx, Capital, Volume II

In other words, the act of buying and selling, however essential for capitalism to function, is not productive in the value-theoretic sense. The merchant who buys goods cheaply and sells them at a markup doesn’t create value through the exchange itself; they merely appropriate a share of value created by productive workers elsewhere.

2. Location in the Circuit of Capital

Capital doesn’t just sit still. It moves through a circuit: it begins as commodities filled with freshly produced surplus value (C’), converts into money through sale in the market (M), and then transforms back into new commodities — raw materials, machinery, labor power — to restart production (C → C’). Activities that feed into this productive cycle — that help produce, maintain, or prepare commodities for the next round of production — sit inside the circuit. Activities that operate outside it (like government services aimed at general welfare, or purely redistributive financial operations) sit outside.

This criterion is critical because it captures something the productive/unproductive distinction alone might miss: even an activity that doesn’t directly produce surplus value can be included if it constitutes an indispensable material precondition for the circuit to continue. Transportation is the classic example — it doesn’t transform a commodity’s physical form, but it physically moves goods to where they’re needed for consumption or further production, which Marx explicitly recognized as a productive act that adds value.

3. Relationship with Surplus Value

The final criterion is the most direct: does this activity produce surplus value, or is it an indispensable condition for surplus value production? If it directly creates value through productive labor, include it. If it’s a necessary supporting activity embedded in the productive circuit, include it. If it merely redistributes value already produced, or operates on entirely different logic (like government), exclude it.

The logic here is that surplus value is the lifeblood of capitalist accumulation. Any sector that doesn’t contribute to its creation or materially enable it is, from the standpoint of the accumulation process, extraneous to the dynamic you’re trying to measure.

The Service Sector Problem

One of the paper’s most valuable theoretical contributions is its treatment of services. When Marx wrote, there was no statistical concept of a “service sector.” Modern macroeconomic data lumps together wildly heterogeneous activities under this label — everything from software development to hairdressing to hospital care.

Gómez Julián, drawing on Tregenna (2009), identifies three types of service activities:

- Those that directly produce surplus value (e.g., software development subcontracted by a manufacturing firm, transportation of goods)

- Those that facilitate surplus value production elsewhere (e.g., warehousing that preserves commodity properties, scientific research contracted by industry)

- Those that remain outside the circuit of capital (e.g., government administration, purely redistributive finance)

This means you cannot simply include or exclude “services” wholesale. Each activity must be examined on its own terms, disaggregated, and asked: does this particular service perform productive labor, or doesn’t it? For “hybrid” sectors that contain both productive and unproductive components, the researcher must determine the proportions and decide based on which dominates.

◆

Applying the Criteria: What’s In, What’s Out

Using Bureau of Economic Analysis data for the United States (1960–2020), Gómez Julián applies these theoretical criteria to 46 consolidated economic sectors. The result is a clear binary classification.

Included — Productive

- Farms

- Forestry, fishing & related activities

- Oil & gas extraction

- Mining (except oil & gas)

- Support activities for mining

- Utilities

- Construction

- All manufacturing (wood, metals, machinery, electronics, motor vehicles, textiles, chemicals, petroleum, paper, printing, plastics, rubber, furniture, food & beverage, apparel, computers, etc.)

- Transportation

- Warehousing & storage

- Information

- Professional, scientific & technical services

- Management of companies & enterprises

- Administrative & waste management services

- Educational services

- Arts, entertainment & recreation

- Accommodation

- Food services & drinking places

- Other services (except government)

Excluded — Non-Productive

- Wholesale trade

- Retail trade

- Finance & insurance

- Real estate

- Rental & leasing services

- Health care & social assistance

- Federal general government

- Federal government enterprises

- State & local general government

- State & local government enterprises

Most of these are straightforward once you accept the theoretical framework. Agriculture, mining, manufacturing — clearly productive. Finance, real estate, government — clearly outside the surplus-value production process. But several borderline cases required careful reasoning.

The Borderline Cases

Warehousing and storage might seem like a pure logistics function, but the paper argues that preserving the physical properties of commodities before they enter the sphere of circulation is a material precondition for their existence as commodities. Without storage, many goods would deteriorate and lose their use-value. This makes warehousing an indispensable part of the productive process, not merely a cost of circulation.

Educational services is perhaps the most controversial inclusion. It encompasses private, public, and non-profit components. The classification system doesn’t specify their proportions. But excluding the sector entirely would mean ignoring a fundamental element for reproducing the skilled labor force in a highly industrialized economy — a cost that productive capital must bear one way or another.

Administrative and waste management services includes activities that generate surplus value (document preparation for productive firms, personnel placement) alongside activities that don’t (security services, household cleaning). The paper argues that since most of the economy consists of productive sectors, and most of these services are contracted by those productive sectors, the productive component likely dominates.

Information produces and distributes cultural products, software, broadcasting content, and data. In accordance with the criteria — these are material products of creative and technical labor, increasingly subcontracted by productive enterprises — it is included.

◆

The Econometric Validation: Three Blind Tests

Here is where the paper’s methodology becomes genuinely innovative. Gómez Julián doesn’t merely propose theoretical criteria and declare victory. He subjects the entire framework to empirical testing using three fundamentally different statistical methods.

A critical point: These econometric methods operate with zero knowledge of Marxist theory. They do not distinguish between “productive” and “unproductive” labor. They have never heard of the circuit of capital. They simply analyze the raw data for all 47 economic sectors and tell you which ones structurally matter for the economy’s behavior. This makes them a powerful independent test — a way to ask the data itself which sectors form the economy’s real core.

Test 1: Principal Component Analysis (PCA)

PCA is a dimensionality reduction technique that identifies the directions (called “principal components”) along which the economy’s sectoral data varies most. Think of it as asking: if the entire economy were a cloud of data points, which directions through that cloud capture the most movement?

Applied to all 47 sectors simultaneously, PCA found that economic variance is highly concentrated: a small number of sectors drive most of the variation, while many others contribute only marginal noise. Using a rigorous statistical criterion — fitting probability distributions to each sector’s contribution and selecting those in the top decile — PCA identified 26 sectors as structurally significant. A post-hoc validation confirmed that none of the 21 excluded sectors had sufficient statistical weight (eigenvalue exceeding 1) to constitute an independent driver.

The first principal component was dominated by corporate and financial services. The second by a logistics-industrial chain. The fourth by extractive natural resources. The seventh by education and public administration.

Test 2: Regularized Horseshoe Regression (RHR)

This Bayesian method uses a “global-local shrinkage” prior that aggressively compresses noise toward zero while preserving strong signals — think of it as a statistical metal detector that ignores pebbles but rings loudly for gold. The name “Horseshoe” is not a metaphor; it refers to the literal U-shaped geometry of the shrinkage coefficient’s probability distribution, which piles mass at the extremes (fully suppress or fully preserve) rather than settling at mediocre intermediate values like conventional methods.

Gómez Julián specified the model to predict total gross operating surplus from total variable capital across all sectors — deliberately grounding the specification in the labor theory of value. The severe multicollinearity inherent in input-output data (sectors move together — when steel production grows, automobile production grows) meant that no individual sector achieved traditional statistical significance. This isn’t a failure. As economists Christopher Achen and Olivier Blanchard have argued, multicollinearity in macroeconomic data is not a “problem” to be fixed with clever statistics; it’s an intrinsic, ontological property of how economies work. Blanchard memorably called it “God’s will.”

What the model could provide was a predictive ranking based on projected predictive density (ELPD): which sectors reduce prediction error fastest. The top 15 sectors identified were:

- Retail Trade

- Textile Mills & Products

- Fabricated Metal Products

- Administrative & Waste Management Services

- Miscellaneous Manufacturing

- Construction

- Educational Services

- Electrical Equipment, Appliances & Components

- Nonmetallic Mineral Products

- Support Activities for Mining

- Printing & Related Support Activities

- Primary Metals

- Food Services & Drinking Places

- State & Local General Government

- Transportation

Test 3: Dynamic Factor Model (DFM)

The DFM extracts hidden “latent factors” from the 47 sectoral time series — unobserved forces that cause sectors to move together. The model found two such factors: one capturing short-term cyclical shocks (low persistence, autoregressive coefficient of 0.33) and one carrying the secular, long-term trend (high persistence, autoregressive coefficient of 0.91). These two factors together explain about 34% of total sectoral variation.

Through an elaborate multi-stage validation involving stability selection, synchronized block bootstrap resampling (300 replications), and a novel “Full-Robust Thresholding” algorithm that generates counterfactual null distributions and corrects for factor indeterminacy via the Hungarian algorithm, the model identified which sectors are most structurally synchronized with these systemic factors.

The sectors with the highest structural weight were: Real Estate, followed by State & Local General Government and Federal General Government, then Retail Trade and Food Services, with Utilities and Chemical Products providing the industrial baseline.

◆

The Key Revelation: Theory and Data Diverge

Now comes the most thought-provoking finding in the paper. The econometric methods — which are purely data-driven and completely agnostic to Marxist theory — identify a set of “core” sectors that overlaps with but also substantially differs from the theoretical classification.

Where Theory and Data Agree

Manufacturing sectors (textiles, metals, fabricated products, miscellaneous manufacturing) appear across multiple econometric methods and are unambiguously included by the theoretical criteria.

Administrative & waste management services ranks 4th in the RHR and is theoretically included as productive.

Educational services appears in the RHR ranking (7th) and is theoretically included.

Transportation appears in the RHR ranking (15th) and is theoretically included.

Construction appears prominently in both RHR (6th) and PCA, and is theoretically included.

Utilities appear in the DFM results and are theoretically included.

These convergences suggest that the theoretical criteria are tracking something real in the data: the sectors that Marx identified as productive are indeed among those that structurally drive the economy.

Where Theory and Data Disagree — And Why It Matters

Real Estate dominates the DFM results (ranked #1 in structural weight) but is theoretically excluded as non-productive and fictitious.

Government sectors (federal and state/local) rank among the top DFM sectors but are theoretically excluded because they don’t pursue profit maximization.

Retail Trade ranks #1 in the RHR and appears prominently in the DFM, yet is theoretically excluded as pure circulation.

Finance & insurance dominate the first principal component in PCA but are theoretically excluded.

Health care has the highest eigenvalue among all excluded sectors in PCA’s post-hoc validation table but is theoretically excluded.

What does this divergence mean? The paper interprets it as profoundly significant. Sectors like real estate, government, and retail trade have “effectively colonized the macro-dynamics of the US rate of profit.” They statistically dominate the national accounting aggregates — they are the forces that shape the observed numbers — even though Marxist theory classifies them as unproductive or revenue-consuming.

In Marx’s own philosophical vocabulary, the phenomenon (what the data shows on its surface) and the essence (what theory identifies as the true engine of value production) diverge. The sectors driving the observable statistical dynamics are not the same as the sectors that, according to the theory, actually generate surplus value. This is not a refutation of either the theory or the data; it’s an insight into how modern capitalism’s surface appearance differs from its underlying structure — exactly as Marx’s own method predicted it would.

◆

Does the Rate of Profit Fall?

With the theoretically selected sectors, all three trend-extraction methods — Daubechies wavelet filters (with 8 vanishing moments at decomposition depth 4), Empirical Mode Decomposition, and the Embedded Hodrick-Prescott filter (implemented within a Bayesian unobserved components model with Gibbs sampling) — produce a clear declining long-term trend in the net average rate of profit over 1960–2020. This is precisely what Marx predicted, and it serves as evidence of the internal consistency of the proposed criteria: the new proposition (the sectoral classification) fits harmoniously within the existing system of Marxist propositions.

For the econometric criteria, the results are remarkably robust: with the single exception of the Hodrick-Prescott filter under the DFM sector selection, all combinations of econometric sector-selection criteria and filtering methods also produce a declining long-term trend. That means:

- PCA sectors + Wavelet → declining

- PCA sectors + EMD → declining

- PCA sectors + HP → declining

- RHR sectors + Wavelet → declining

- RHR sectors + EMD → declining

- RHR sectors + HP → declining

- DFM sectors + Wavelet → declining

- DFM sectors + EMD → declining

- DFM sectors + HP → not clearly declining

Regardless of which sectors you choose — based on careful Marxist reasoning or on pure data analysis — and regardless of which statistical filter you use, the long-term profit rate falls. The HP-DFM exception is attributed to the filter’s parametric specifications (its linear structure and second-order Markov assumption for the trend) potentially interacting poorly with a sectoral composition heavily weighted toward government and real estate — sectors whose dynamics may follow different logics than productive capital.

The Empirical Mode Decomposition, being a non-parametric technique that adapts to the data’s intrinsic patterns without imposing prior assumptions about functional form, consistently produced the most accentuated declining trend across all sector selections.

◆

Why This Paper Matters

Gómez Julián’s work makes three contributions that will resonate well beyond the boundaries of Marxist economics:

First, methodological standardization. For the first time, there is a theoretically grounded, explicit, and reproducible set of criteria for deciding which sectors belong in Marxist profit-rate calculations. This addresses a four-decade-old methodological gap and enables meaningful comparison across future studies. Researchers can now reproduce the same classification, apply it to different countries or time periods, and test whether the declining tendency holds universally.

Second, the theory-data tension as an analytical asset. Rather than hiding the divergence between theoretical classifications and empirical results, the paper treats it as a finding in its own right. The fact that unproductive sectors statistically dominate the macro-dynamics of the profit rate tells us something important about how modern capitalism appears on its surface versus how it functions at its core. It demonstrates, empirically, that Marx’s concept of “essence” and “phenomenon” isn’t merely philosophical abstraction — it describes a real, measurable gap in economic data.

Third, the robustness of the declining trend. Whether you select sectors based on careful Marxist reasoning or let unsupervised statistical methods decide for you, the long-term profit rate declines. This convergence across radically different methodologies strengthens the empirical case for what may be Marx’s most famous — and most contested — prediction.

The paper does not claim to have proven Marx right beyond doubt. Internal consistency, it notes, does not guarantee overall theoretical validity. But it has demonstrated that when you take the theory seriously — when you build your measurement instrument to match the conceptual categories rather than stuffing everything into the equation and hoping for the best — the data speaks in a direction that Marx would have recognized.