Can We Manage Fixed Capital Surpluses Without Money?

An economist revisits a passage Marx left half-finished and asks: what if a post-capitalist society had to balance its machines, factories, and tools—without printing a single banknote?

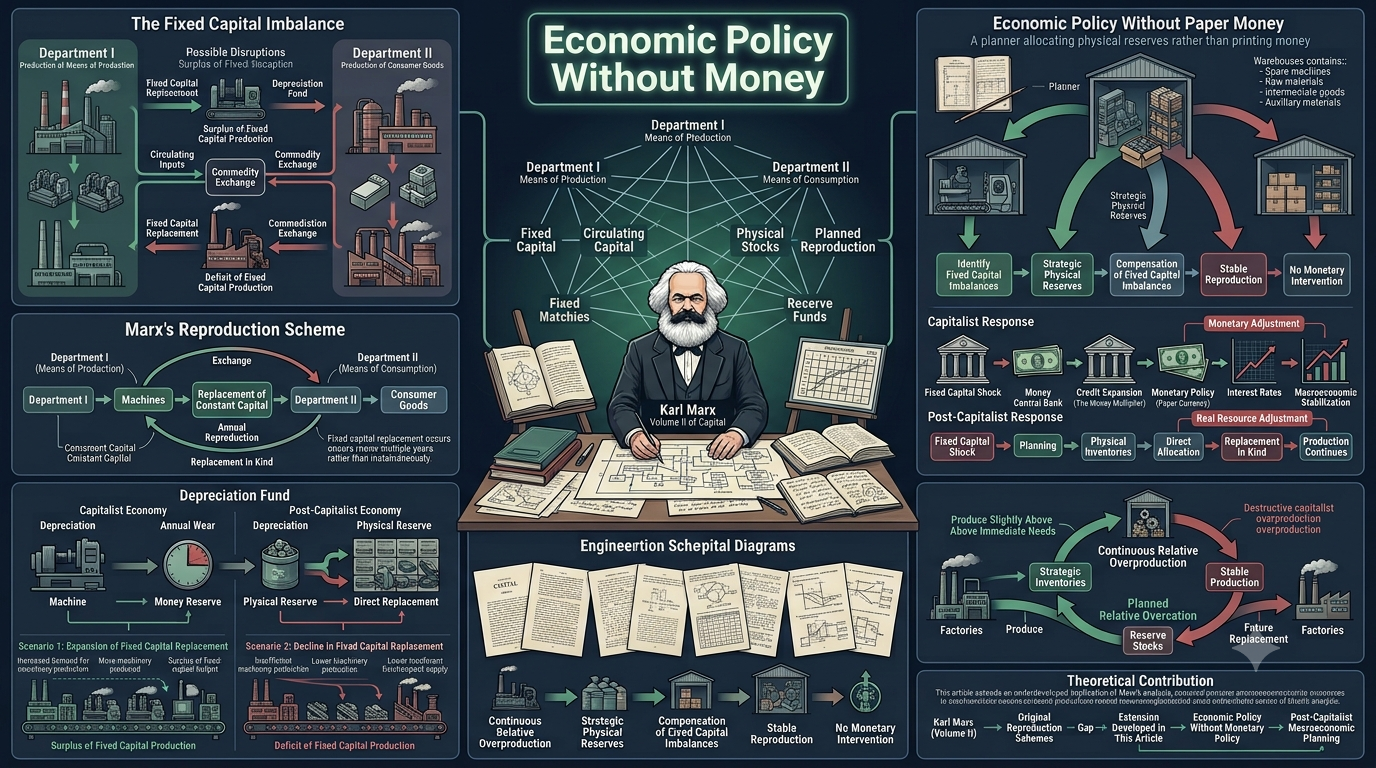

Most of us think of money as the universal lubricant of an economy—the thing that lets a shoe factory buy steel, and the steel mill pay its workers. But what happens when an economy decides it no longer needs money? Can it still keep its machines, buildings, and equipment in balance? That is the question José Mauricio Gómez Julián tackles in a compact, ambitious paper that draws directly on Karl Marx’s Capital, Volume II.

Why Fixed Capital Matters

Before diving in, let’s clarify what “fixed capital” means. In economics—especially in the Marxian tradition—a factory’s resources are split into two broad categories. Circulating capital is the stuff that gets used up quickly in production: raw materials, intermediate goods, energy. Fixed capital is the durable stuff—machinery, buildings, infrastructure—that transfers its value to the product gradually, over many production cycles, through wear and tear (what economists call “depreciation”).

In any economy, these two types of capital need to exist in the right proportion. Too much fixed capital relative to circulating capital, and the machines sit idle for lack of materials. Too little, and the raw materials pile up with nothing to process them. Getting this ratio wrong creates either a surplus (overproduction of fixed capital) or a deficit (underproduction of fixed capital).

The Two Scenarios: Surplus and Deficit

Gómez Julián works through two thought experiments, both grounded in Marx’s two-sector model of reproduction (Sector I produces means of production—factories, machines; Sector II produces consumer goods). The logic is dense, but the intuition is elegant.

Scenario One

Suppose the fixed capital used by the consumer-goods sector (Sector II) depreciates faster than expected in a given year. More machines need replacing now. Sector I sends more fixed-capital goods to Sector II, but its overall output for Sector II remains the same. The result: Sector I now produces more fixed capital than Sector II can absorb, while simultaneously Sector II needs less circulating capital (raw materials) because it is replacing machines rather than running them.

Scenario Two

Now imagine the opposite: a smaller portion of Sector II’s fixed capital needs to be physically replaced this year (because less has worn out completely). That means less demand for new fixed-capital goods from Sector I. Meanwhile, the circulating capital flows remain unchanged. Sector I simply produces fewer fixed-capital items.

In a capitalist economy, these imbalances ripple outward. The surplus scenario pushes more money into Sector I (as depreciation funds accumulate), but the actual exchange of goods shrinks. Money becomes a one-sided “means of purchase” rather than a smooth intermediary. In the deficit scenario, production contracts. Both situations, if left unmanaged, can trigger commercial crises—and in capitalism, those crises are cyclical, not one-off events.

The Money Question

Here is where the paper gets provocative. In a capitalist system, managing these imbalances requires monetary policy—central banks adjusting interest rates, governments running deficits, currencies being devalued. The entire toolkit of modern macroeconomics is, in one way or another, about using money to smooth out the frictions between production and exchange.

But Gómez Julián asks: what if you remove money from the equation entirely? What if a post-capitalist society—one that has moved beyond the commodity form—tries to manage fixed capital imbalances without any monetary instrument at all?

The logic works like this. If fixed capital wears out unevenly from year to year (sometimes more, sometimes less), a well-organized post-capitalist economy could buffer those fluctuations by maintaining reserve stocks of both fixed-capital goods and circulating-capital goods. When a year of heavy depreciation hits, the reserve steps in. When a year of light depreciation comes, the reserve grows. The goal is not maximum efficiency at every moment, but stability over time—a kind of industrial shock absorber.

Why This Is Harder Than It Sounds

The author is careful to note that this approach would be catastrophic in a capitalist economy. Continuous relative overproduction, without the discipline of a planned system, would generate commercial crises—overproduction in capitalism is not a “reserve strategy” but a trigger for collapse. The same policy looks entirely different depending on whether production is coordinated through market exchange or through conscious social planning.

This is the key theoretical distinction: in a planned economy, overproduction is relative (producing more than immediate need, but deliberately) and continuous (a permanent buffer). In capitalism, overproduction is absolute (goods that cannot find buyers) and cyclical (recurring crises). Same material fact, radically different systemic consequences.

A Critique the Author Couldn’t Ignore

The paper ends with a sharp jab at Soviet Marxist economics. Gómez Julián points out that the standard Soviet reference text—the Dictionary of Marxist Political Economy by Borisov, Zhamin, and Makárova (1965)—never develops, or even mentions, this particular theoretical problem. The analysis is absent from the entries on “Fixed Capital,” “Simple Reproduction,” and “Extended Reproduction.” Marx himself only sketched it in embryonic form (Volume II, pp. 414–417), yet the author argues it is a “vital” issue for any theory of post-capitalist construction.

His verdict on Soviet scholarship is unsparing: the Soviet economists, he suggests, never truly understood many of the theoretical foundations they claimed to be building on—a failure that history confirmed on November 9, 1989.

Why This Paper Deserves Your Attention

You do not have to be a Marxist to find this paper interesting. At its heart, it is about a problem that any complex economy faces: how do you keep the right balance between durable infrastructure and the materials that flow through it? Modern economies answer this with monetary policy, fiscal stimulus, and market signals. Gómez Julián asks whether a fundamentally different kind of society could answer it with strategic reserves and conscious planning instead.

Whether or not you find his vision persuasive, the thought experiment sharpens something important: our reliance on money as an economic management tool is not a law of nature—it is a feature of a particular system. And understanding why that system needs money is the first step toward imagining alternatives, or toward improving what we already have.

Read the full paper here: https://dialnet.unirioja.es/servlet/articulo?codigo=9041512